December 8, 2015

Cheniere Energy, Inc.

Wells Fargo Energy Symposium

Forward Looking Statements

This presentation contains certain statements that are, or may be deemed to be, “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as

amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, included or incorporated by reference herein

are “forward-looking statements.” Included among “forward-looking statements” are, among other things:

statements regarding the ability of Cheniere Energy Partners, L.P. to pay distributions to its unitholders or Cheniere Energy Partners LP Holdings, LLC to pay dividends to its

shareholders;

statements regarding Cheniere Energy Inc.’s, Cheniere Energy Partners LP Holdings, LLC’s or Cheniere Energy Partners, L.P.’s expected receipt of cash distributions from their

respective subsidiaries;

statements that Cheniere Energy Partners, L.P. expects to commence or complete construction of its proposed liquefied natural gas (“LNG”) terminals, liquefaction facilities,

pipeline facilities or other projects, or any expansions thereof, by certain dates or at all;

statements that Cheniere Energy, Inc. expects to commence or complete construction of its proposed LNG terminals, liquefaction facilities, pipeline facilities or other

projects by certain dates or at all;

statements regarding future levels of domestic and international natural gas production, supply or consumption or future levels of LNG imports into or exports from North

America and other countries worldwide, or purchases of natural gas, regardless of the source of such information, or the transportation or other infrastructure, or demand

for and prices related to natural gas, LNG or other hydrocarbon products;

statements regarding any financing transactions or arrangements, or ability to enter into such transactions;

statements relating to the construction of our proposed liquefaction facilities and natural gas liquefaction trains (“Trains”), or modifications to the Creole Trail Pipeline,

including statements concerning the engagement of any engineering, procurement and construction ("EPC") contractor or other contractor and the anticipated terms and

provisions of any agreement with any EPC or other contractor, and anticipated costs related thereto;

statements regarding any agreement to be entered into or performed substantially in the future, including any revenues anticipated to be received and the anticipated

timing thereof, and statements regarding the amounts of total LNG regasification, liquefaction or storage capacities that are, or may become, subject to contracts;

statements regarding counterparties to our commercial contracts, construction contracts and other contracts;

statements regarding our planned development and construction of additional Trains, including the financing of such Trains;

statements that our Trains, when completed, will have certain characteristics, including amounts of liquefaction capacities;

statements regarding our business strategy, our strengths, our business and operation plans or any other plans, forecasts, projections or objectives, including anticipated

revenues and capital expenditures and EBITDA, any or all of which are subject to change;

statements regarding projections of revenues, expenses, earnings or losses, working capital or other financial items;

statements regarding legislative, governmental, regulatory, administrative or other public body actions, approvals, requirements, permits, applications, filings,

investigations, proceedings or decisions;

statements regarding our anticipated LNG and natural gas marketing activities; and

any other statements that relate to non-historical or future information.

These forward-looking statements are often identified by the use of terms and phrases such as “achieve,” “anticipate,” “believe,” “contemplate,” “develop,” “estimate,” “example,”

“expect,” “forecast,” “goals,” “opportunities,” “plan,” “potential,” “project,” “propose,” “subject to,” “strategy,” “target,” and similar terms and phrases, or by use of future tense.

Although we believe that the expectations reflected in these forward-looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these expectations

may prove to be incorrect. You should not place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. Our actual results could

differ materially from those anticipated in these forward-looking statements as a result of a variety of factors, including those discussed in “Risk Factors” in the Cheniere Energy, Inc.,

Cheniere Energy Partners, L.P. and Cheniere Energy Partners LP Holdings, LLC Annual Reports on Form 10-K filed with the SEC on February 20, 2015, which are incorporated by

reference into this presentation. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these ”Risk Factors.” These

forward-looking statements are made as of the date of this presentation, and other than as required under the securities laws, we undertake no obligation to publicly update or revise

any forward-looking statements.

2

Executing on Strategy

2025 Forecast for CEI

Flexible,

Scalable,

industry-

leading

platform

$50B+

~60 mtpa

LNG by

2025

One of the largest

natural gas buyers in

the U.S.

~9 Bcf/d

Supporting over

200,000 indirect jobs

~1,000

permanent

jobs created

One of the largest

exporters of LNG on

a global basis

~14%

of the

total LNG market

in U.S.

infrastructure

Significant investment

in U.S. infrastructure

3

Cheniere’s Key Businesses

Four planned LNG

terminals to be

located along Gulf

of Mexico

~60 mtpa planned

Scalable platform

SPL T1-5 and CCL 1-

2 underpinned by

long-term contracts,

competitive capital

costs

LNG sales, FOB or

DES, provided to

customers on a

short, mid, and

long-term basis

~9 mtpa LNG

volumes expected

from SPL T1-6 and

CCL T1-3

3 chartered LNG

vessels to date

Developing/

investing in

infrastructure to

facilitate

hydrocarbon

revolution in Texas

and beyond

Optimize value of

LNG platform

Identify

opportunities in

related markets

Providing feedstock

for LNG production

Redundant pipeline

capacity ensures

reliable gas

deliverability

Upstream pipeline

capacity provides

access to diverse

supply sources

LNG

PLATFORM

GAS

PROCUREMENT

CHENIERE

MARKETING

FUTURE

DEVELOPMENTS

4

Projected Global LNG Demand 436 mtpa by 2025

22 19 23

2015

2020 2025

2015 2020 2025

6

10 17

2015 2020

2025

2015 2020 2025

Americas

Asia

Middle East/N. Africa

184

260

305

31

78

92

Europe

Source: Wood Mackenzie

Q3 2015 LNG Tool

(1) Assumes 85% utilization of nameplate capacity

Demand forecasted to increase by 193 mtpa to 2025, a 6% CAGR

Average of 23 mtpa of new liquefaction capacity needed each year

(1)

5

U.S. Expected To Become One of the Top Three LNG Suppliers

Projected LNG Liquefaction Capacity

2014 Global LNG Liquefaction Capacity: ~37 Bcf/d

6

United States

77

mtpa

68

mtpa

Qatar

Source: Wood Mackenzie Q3 2015

Cheniere

2014 2025

2014

2025

2014

2025

MEG

MEG

Rest of World

Includes Existing and

Under Construction

Projects

2014: 171 mtpa

2025: 189 mtpa

AB

2014

2025

AB

AP

AP

1.4

mtpa

26

mtpa

81

mtpa

Australia

Cheniere

Sabine Pass T1-6

Corpus Christi T1-5

Parallax

2025

64

mtpa

under

const.

31.5

mtpa

under

const.

94

mtpa

60

mtpa

Cheniere LNG Platform

Sabine Pass

Liquefaction

TX

LA

Creole Trail PL

Sabine Pass Liquefaction

• 6 train development – 27 mtpa

(~3.8 Bcf/d in export capacity)

• Trains 1-5 are under construction;

First LNG expected in late 2015

• Train 6 under development,

FID expected 2015/16

Corpus Christi

Liquefaction

7

Corpus Christi Liquefaction

• 5 train development – 22.5 mtpa

(~3.2 Bcf/d in export capacity)

• Trains 1-2 are under construction; First

LNG expected in late 2018

• Train 3 under development; FID

expected 2015/16

• Trains 4-5 under development;

Permitting process initiated June 2015

Live Oak

LNG

Live Oak LNG

1

• ~5 mtpa development

(~0.8Bcf/d)

• First LNG targeted in late 2021

Louisiana LNG

1

• ~5 mtpa development

(~0.7Bcf/d)

• First LNG targeted in late 2021

Louisiana

LNG

Under Construction

Proposed

(1) Cheniere Energy, Inc. has agreed in principle to partner with Parallax Enterprises, LLC on these projects

Aerial View of SPL Construction – August 2015

Train 1

Train 3

Train 4

Propane Condenser Area

T2 Ethylene Cold Box

T2 Methane Cold Box

Train 2

Air Coolers

T1 Methane Cold Box

T1 Ethylene Cold Box

T3 Ethylene Cold Box

T3 Methane Cold Box

Train 5

T5 Soil Stabilization

Train 6 Under Development

Forecast Cheniere LNG Portfolio Summary

Approximately 87% of LNG volumes for trains under construction are underpinned with LT

SPAs, cash flows support current project debt of $21.5B

20-year LT SPAs with investment-grade counterparties

For the balance of LNG volumes, long-term contracts are no longer required; Cheniere

expects to sell LNG under shorter-term contracts or on a spot basis

9

SPL

Trains 1

-

6

CCL

Trains 1

-

3

Total

CCL

Trains 4

-

5

LO &

LLNG

1

Total

Design Capacity

27.0 13.5 40.5 9.0 ~10 ~59.5

Under Construction

(underpinned by LT SPAs)

22.5

(~88% sold)

9.0

(~85% sold)

31.5

(~87% sold)

In Permitting

In Permitting

31.5

(~87% sold)

LT SPAs Target

(sold to date)

21.25

(19.8 )

10.5

(8.4)

31.75

(28.2)

- -

31.75

(28.2)

Excess Volumes:

Customized

Contracts/CMI

5.75 3.0 8.75 9.0 ~10 ~27.75

EBITDA is a non-GAAP measure. EBITDA is computed as total revenues less non-cash deferred revenues, operating expenses, assumed commissioning costs and state and local taxes. It does not include

depreciation expenses and certain non-operating items. We have not made any forecast of net income, which would be the most comparable financial measure under GAAP, and we are unable to

reconcile differences between forecasted EBITDA and net income. EBITDA has limitations as an analytical tool and should not be considered in isolation or in lieu of an analysis of our results as

reported under GAAP, and should be evaluated only on a supplementary basis.

(in MTPA)

(1) Cheniere Energy, Inc. has agreed in principle to partner with Parallax Enterprises, LLC on these projects

Cheniere’s LNG Export Projects

Underpinned with Attractive SPA Features

10

Proven record of execution; proven technology

SPAs feature parent guarantees & HH + fixed fee (no price reopeners)

Cheniere LNG SPAs: LNG price tied to Henry Hub, destination flexibility,

upstream gas procurement services, no lifting requirements

$7.7

$9.5

$12.0

$14.0

$14.5

$13.0

$8.4

$11.5

$13.0

$16.0

$17.0

$18.5

$5

$10

$15

$20

Cheniere Gulf Coast West Africa Western Canada Northwest Australia East Africa Southeast Asia

LNG prices ($/MMBtu)

Cheniere Offers Competitive, Low Cost Source of LNG

The U.S. is one of the lowest cost natural gas providers in the world

U.S. liquefaction project costs are also significantly lower due to less project

development needed

The breakeven LNG price for Cheniere LNG export facilities is one of the lowest

compared to other proposed LNG projects

11

Estimated b

reakeven LNG pricing range, Delivered Ex-Ship to Asia

Source: Cheniere Research, Wood Mackenzie, company filings and investor materials.

Note: Breakeven prices derived assuming unlevered after-tax returns of 10% on Canadian projects and 12% on all other projects over construction plus 20 years of operation. Henry Hub at $3.00/MMBtu

($ in billions, except for per share amounts)

Corpus Christi

(CCL T1-2)

Total CEI standalone

CEI cash flow build up (2021 estimated amounts)

Project EBITDA / Deconsolidated for standalone $3.0 $1.3 $4.3 $2.3

Less: Project-level interest expense ($1.0) ($0.5) ($1.5) ($0.5)

Distributable cash flow from project $2.1 $0.8 $2.9 $1.8

% cash flows to CEI (Adjusted for minority interests) 49% 100%

Project cash flows to CEI (Adjusted for minority interests) $1.0 $0.8 $1.8

Total project cash flows to CEI $1.0 $0.8 $1.8

Plus: Management fees to CEI $0.1

Less: CEI G&A ($0.3)

Less: CEI-level interest expense ($0.0)

CEI cash flow $1.6

CEI cash flow per share $6

Current debt outstanding

SPL and CCL project-level debt outstanding

(2)

$13.1 $8.4 $21.5 –

SPLNG and CTPL project-level debt outstanding $2.5 – $2.5 –

CEI-level debt outstanding – – – $0.6

Total debt outstanding $15.6 $8.4 $24.0 $0.6

CQP

(SPL T1-5/SPLNG/CTPL)

(1)

(3)

(3)

(3)

(1)

(1)

7-train CEI cash flow estimate – Current market snapshot

SPL T1-5, CCL T1-2

7

-train CEI cash flow estimate – Current market snapshot | SPL T1-5, CCL T1-2

7 trains currently under construction financed with non-recourse project level debt – SPL T1-5 (CQP) and CCL T1-2 (CEI)

Based on 27.4 MTPA of 20-year SPAs; assumes remaining LNG sold to Europe at current market prices and shipping rates –

NBP price of $6.32/MMBtu, Henry Hub price of $2.54/MMBtu, shipping day rates of $30,000/day

(4)

For scenario shown above, estimated income tax payments of ~15% of CEI pre-tax cash flow projected to start in 2023/24

12

Note: See “Forward Looking Statements” slide. Cash flow build up scenario above assumes refinancing of SPL and CCH credit facilities with non-amortizing project bonds.

SPL, SPLNG, CTPL and CCL-level project debt shown above are non-recourse to CEI.

EBITDA, distributable cash flow, deconsolidated cash flow, cash flow and cash flow per share are non-GAAP measures. EBITDA is computed as total revenues less non-cash deferred revenues, operating expenses,

assumed commissioning costs and state and local taxes. It does not include depreciation expenses and certain non-operating items. We have not made any forecast of net income, which would be the most

comparable financial measure under GAAP, and we are unable to reconcile differences between forecasted non-GAAP measures and net income. Non-GAAP measures have limitations as an analytical tool and

should not be considered in isolation or in lieu of an analysis of our results as reported under GAAP, and should be evaluated only on a supplementary basis.

(1) ~$2.3 billion of deconsolidated cash flow to CEI calculated as ~$1.0 billion of CQP distributable cash flow (net of minority interest), plus ~$1.3 billion of CCL Trains 1‐2 EBITDA. CEI stand‐alone EBITDA is

estimated to be ~$2.1 billion calculated as ~$2.3 billion of deconsolidated cash flow to CEI, plus $0.1 billion of management fees, less ~$0.3 billion of CEI G&A.

(2) CCL project-level debt issued at Cheniere Corpus Christi Holdings, LLC (CCH) entity.

(3) Assumes ~276 million CEI shares outstanding for 7-train case – assumes conversion of $1.0 billion PIK Convertible Notes due in 2021 at $93.64/share and conversion of $1.0 billion Senior Secured Convertible

Notes due 2025 at $100/share.

(4) Source: Bloomberg, DTN ProphetX and Platts, as of October 13, 2015.

Estimated Market Prices Profitable for Cheniere LNG Projects

13

As shown in sensitivity table above, Cheniere can profitably sell LNG into key demand centers

even in periods of lower market prices

If LNG prices remain at lower levels, we would expect LNG demand to increase, thus signaling

the need for more liquefaction projects. Cheniere positioned as a low-cost supplier

Cheniere can profitably provide LNG to global buyers at attractive prices

Assumes Henry Hub price of $3.00/MMBtu, shipping cost to Europe of $1.00/MMBtu and shipping cost to Asia of $2.25/MMBtu.

Market price sensitivity

Europe LNG

sale price ($/MMBtu)

$7.00

$9.00

$11.00

$13.00

Implied margin

$2.50

$4.50

$6.50

$8.50

Asia LNG

sale price ($/MMBtu

)

$9.00

$11.00

$13.00

$15.00

Implied margin

$3.25

$5.25

$7.25

$9.25

($ in billions, except for per share amounts)

Run-rate scenarios from 2021E to 2025E

7 trains

(2021E)

9 trains

(2021E)

11 trains

(2023E)

11 trains,LO&LLNG

(2025E)

SPL T1-5/6 and SPLNG via GP/IDR and CQH $1.1 $1.3 $1.3 $1.3

Management fees $0.1 $0.1 $0.1 $0.2

Mid-scale LNG – – – $1.2

CCL T1-2/3/5 $1.3 $2.0 $3.4 $3.4

CMI profit share – – – –

Total $2.5 $3.5 $4.8 $6.1

Less: CEI G&A ($0.3) ($0.3) ($0.3) ($0.3)

CEI EBITDA $2.2 $3.2 $4.6 $5.8

CEI EBITDA per share $8 $11 $16 $20

Example CEI EBITDA Build Up – Europe @ $7.50 / Asia @ $8.75

SPL T1-6, CCL T1-3, CCL T4-5, Live Oak/Louisiana LNG

CEI EBITDA build up (deconsolidated)

7 trains currently under construction

7-train case assumes 27.4 MTPA of 20-year SPAs; all other build out cases assume 31.75 MTPA of 20-year SPAs

Assumes remaining LNG all sold to Europe for $7.50/MMBtu or Asia for $8.75/MMBtu

14

Note: See “Forward Looking Statements” Slide.

Cash flow build up scenario above assumes refinancing of SPL and CCH credit facilities with non-amortizing project bonds and early release of SPL cash flows earmarked for construction via public CQP unit issuances.

Cash flow build up scenario above requires either incremental CEI, or project-level financing, or combination of both, to fund project build out. Assumes ~276 million CEI shares outstanding for 7-train case – assumes

conversion of $1.0 billion PIK Convertible Notes due in 2021 at $93.64/share and conversion of $1.0 billion Senior Secured Convertible Notes due 2025 at $100/share. All other cases shown assume ~283 million CEI

shares outstanding – incremental shares related to funding of committed additional $0.5 billion of Senior Secured Convertible Notes due 2025 and conversion at $140/share.

EBITDA and EBITDA per share are non-GAAP measures. EBITDA is computed as total revenues less non-cash deferred revenues, operating expenses, assumed commissioning costs and state and local taxes. It does not

include depreciation expenses and certain non-operating items. We have not made any forecast of net income, which would be the most comparable financial measure under GAAP, and we are unable to reconcile

differences between forecasted EBITDA and net income. EBITDA has limitations as an analytical tool and should not be considered in isolation or in lieu of an analysis of our results as reported under GAAP, and

should be evaluated only on a supplementary basis.

Estimates based on assessment of current and potential future project development opportunities, which, among other things, would require acceptable commercial and financing arrangements, and may require

regulatory approvals before we make final investment decisions. Actual performance may differ materially from the goals. Assumes future long term contracting of additional ~2.1 MTPA at CCL Train 3 (total of 10.5

MTPA of long term SPAs at CCL Trains 1-3), 1.5 MTPA at SPL Train 6 (total of 21.25 MTPA of long term SPAs at SPL Trains 1-6) at $3.50 per MMBtu. For illustrative purposes; assumes excess volumes sold by CMI at

above prices.

•For 9 train build out, 8.75 MTPA available for CMI portfolio. For 11 train build out, incremental 9.0 MTPA available for CMI.

•With mid-scale LNG projects, incremental 10.4 MTPA available for CMI.

•All scenarios assume 100% utilization of capacity available.

($ in billions, except for per share amounts)

Run-rate scenarios from 2021E to 2025E

7 trains

(2021E)

9 trains

(2021E)

11 trains

(2023E)

11 trains,LO&LLNG

(2025E)

SPL T1-5/6 and SPLNG via GP/IDR and CQH $1.1 $1.3 $1.3 $1.3

Management fees $0.1 $0.1 $0.1 $0.2

Mid-scale LNG – – – $2.3

CCL T1-2/3/5 $1.3 $2.0 $3.4 $3.4

CMI profit share $0.4 $0.9 $1.9 $1.9

Total $2.9 $4.4 $6.7 $9.0

Less: CEI G&A ($0.3) ($0.3) ($0.3) ($0.3)

CEI EBITDA $2.6 $4.1 $6.4 $8.7

CEI EBITDA per share $9 $14 $23 $31

Example CEI EBITDA Build Up – Europe @ $9.50 / Asia @ $10.75

SPL T1-6, CCL T1-3, CCL T4-5, Live Oak/Louisiana LNG

15

7 trains currently under construction

7-train case assumes 27.4 MTPA of 20-year SPAs; all other build out cases assume 31.75 MTPA of 20-year SPAs

Assumes remaining LNG all sold to Europe for $9.50/MMBtu and Asia for $10.75/MMBtu

CEI EBITDA build up (deconsolidated)

15

Note: See “Forward Looking Statements” Slide.

Cash flow build up scenario above assumes refinancing of SPL and CCH credit facilities with non-amortizing project bonds and early release of SPL cash flows earmarked for construction via public CQP unit issuances.

Cash flow build up scenario above requires either incremental CEI, or project-level financing, or combination of both, to fund project build out. Assumes ~276 million CEI shares outstanding for 7-train case – assumes

conversion of $1.0 billion PIK Convertible Notes due in 2021 at $93.64/share and conversion of $1.0 billion Senior Secured Convertible Notes due 2025 at $100/share. All other cases shown assume ~283 million CEI

shares outstanding – incremental shares related to funding of committed additional $0.5 billion of Senior Secured Convertible Notes due 2025 and conversion at $140/share.

EBITDA and EBITDA per share are non-GAAP measures. EBITDA is computed as total revenues less non-cash deferred revenues, operating expenses, assumed commissioning costs and state and local taxes. It does not

include depreciation expenses and certain non-operating items. We have not made any forecast of net income, which would be the most comparable financial measure under GAAP, and we are unable to reconcile

differences between forecasted EBITDA and net income. EBITDA has limitations as an analytical tool and should not be considered in isolation or in lieu of an analysis of our results as reported under GAAP, and

should be evaluated only on a supplementary basis.

Estimates based on assessment of current and potential future project development opportunities, which, among other things, would require acceptable commercial and financing arrangements, and may require

regulatory approvals before we make final investment decisions. Actual performance may differ materially from the goals. Assumes future long term contracting of additional ~2.1 MTPA at CCL Train 3 (total of 10.5

MTPA of long term SPAs at CCL Trains 1-3), 1.5 MTPA at SPL Train 6 (total of 21.25 MTPA of long term SPAs at SPL Trains 1-6) at $3.50 per MMBtu. For illustrative purposes; assumes excess volumes sold by CMI at

above prices.

•For 9 train build out, 8.75 MTPA available for CMI portfolio. For 11 train build out, incremental 9.0 MTPA available for CMI.

•With mid-scale LNG projects, incremental 10.4 MTPA available for CMI.

•All scenarios assume 100% utilization of capacity available.

($ in billions, except for per share amounts)

Run-rate scenarios from 2021E to 2025E

7 trains

(2021E)

9 trains

(2021E)

11 trains

(2023E)

11 trains,LO&LLNG

(2025E)

SPL T1-5/6 and SPLNG via GP/IDR and CQH $1.1 $1.3 $1.3 $1.3

Management fees $0.1 $0.1 $0.1 $0.2

Mid-scale LNG – – – $3.4

CCL T1-2/3/5 $1.3 $2.0 $3.4 $3.4

CMI profit share $0.9 $1.8 $3.7 $3.7

Total $3.3 $5.3 $8.6 $11.9

Less: CEI G&A ($0.3) ($0.3) ($0.3) ($0.3)

CEI EBITDA $3.0 $5.0 $8.3 $11.6

CEI EBITDA per share $11 $18 $29 $41

Example CEI EBITDA Build Up – Europe @ $11.50 / Asia @ $12.75

SPL T1-6, CCL T1-3, CCL T4-5, Live Oak/Louisiana LNG

16

CEI EBITDA build up (deconsolidated)

7 trains currently under construction

7-train case assumes 27.4 MTPA of 20-year SPAs; all other build out cases assume 31.75 MTPA of 20-year SPAs

Assumes remaining LNG all sold to Europe for $11.50/MMBtu and Asia for $12.75/MMBtu

16

Note: See “Forward Looking Statements” Slide.

Cash flow build up scenario above assumes refinancing of SPL and CCH credit facilities with non-amortizing project bonds and early release of SPL cash flows earmarked for construction via public CQP unit issuances.

Cash flow build up scenario above requires either incremental CEI, or project-level financing, or combination of both, to fund project build out. Assumes ~276 million CEI shares outstanding for 7-train case – assumes

conversion of $1.0 billion PIK Convertible Notes due in 2021 at $93.64/share and conversion of $1.0 billion Senior Secured Convertible Notes due 2025 at $100/share. All other cases shown assume ~283 million CEI

shares outstanding – incremental shares related to funding of committed additional $0.5 billion of Senior Secured Convertible Notes due 2025 and conversion at $140/share.

EBITDA and EBITDA per share are non-GAAP measures. EBITDA is computed as total revenues less non-cash deferred revenues, operating expenses, assumed commissioning costs and state and local taxes. It does not

include depreciation expenses and certain non-operating items. We have not made any forecast of net income, which would be the most comparable financial measure under GAAP, and we are unable to reconcile

differences between forecasted EBITDA and net income. EBITDA has limitations as an analytical tool and should not be considered in isolation or in lieu of an analysis of our results as reported under GAAP, and

should be evaluated only on a supplementary basis.

Estimates based on assessment of current and potential future project development opportunities, which, among other things, would require acceptable commercial and financing arrangements, and may require

regulatory approvals before we make final investment decisions. Actual performance may differ materially from the goals. Assumes future long term contracting of additional ~2.1 MTPA at CCL Train 3 (total of 10.5

MTPA of long term SPAs at CCL Trains 1-3), 1.5 MTPA at SPL Train 6 (total of 21.25 MTPA of long term SPAs at SPL Trains 1-6) at $3.50 per MMBtu. For illustrative purposes; assumes excess volumes sold by CMI at

above prices.

•For 9 train build out, 8.75 MTPA available for CMI portfolio. For 11 train build out, incremental 9.0 MTPA available for CMI.

•With mid-scale LNG projects, incremental 10.4 MTPA available for CMI.

•All scenarios assume 100% utilization of capacity available.

Gas Procurement

Sabine Pass Terminal

Securing feedstock for LNG

production with balanced

portfolio approach

• To date, have entered into term

gas supply contracts with

producers under 1-7 year

contracts

• Supply contracts cover ~50% of

the required daily load for Trains

1-4 at Sabine Pass

• Pricing averages HH - $0.10

discount

Redundant pipeline capacity helps ensure reliable gas deliverability

• To date, we have secured firm pipeline transportation capacity of

approximately ~4.2 Bcf/d of deliverability into Sabine Pass, or ~160% of the

total load for Trains 1-4

Upstream pipeline capacity provides access to diverse supply sources

• High degree of visibility into our ability to consistently deliver gas to Sabine

Pass on a variable basis at Henry Hub flat

17

Shale Plays

Basins

Source: Lippman Consulting, Baker Hughes and Bentek, as of January 2014

NGPL

Tennessee Gas

HPL

KM Tejas

Oasis

Enterprise

Permian

Basin

Barnett

Granite

Wash

Eagle Ford

Haynesville

Marcellus /

Utica

Corpus Christi

Woodford

Gas Procurement

Corpus Christi Terminal

CCL contracting long-term direct and

upstream pipeline transport capacity

• Tennessee P/L: 0.3 Bcf/d

• KM Tejas P/L: 0.25 Bcf/d

• NGPL P/L: 0.385 Bcf/d

CCL purchasing natural gas from producers

and marketers

18

Cheniere Marketing

Scale up for > 10 mtpa including LNG

purchases from Cheniere terminals and

other places

Buyers & sellers of LNG cargoes

SPAs with SPL and CCL for all LNG

volumes not sold to 3

rd

parties

Chartered 3 LNG vessels for deliveries

in 2015 and 2016 (1

st

vessel received

June 2015)

Developing complementary,

high-value markets through

small-scale asset investments

Professional staff based in London,

Houston, Washington, Santiago, and

Singapore

~340 million MMBtu sold to date

primarily based on 1–2 year terms at

prices linked to HH or TTF

Cheniere platform for LNG sales - short, mid, long-term sales, FOB or DES basis

Singapore

Houston, TX

Santiago, Chile

London, U.K.

Chartered 3 LNG Vessels SPA with SPL SPAs with CCL

Deliveries in 2015 & 2016 First LNG for SPL Expected 2015 First LNG Expected 2018

19

Washington, D.C.

Future Developments

Horizontal / Vertical Integration

Total focus

on cash

flow per

share as

guiding

metric for

future

investments

Announced

brownfield

expansion at

Corpus

Christi and

mid-scale

LNG

investment

Significant

revenue

expected

starting in

2016

Cheniere core competencies, scale, and first-mover advantage

provide industry-leading platform for further asset integration

Developing

additional

assets for

other

hydrocarbon

export

opportunities

20

Appendix

Investing in Cheniere – Summary Organization

Cheniere Energy, Inc.

(NYSE MKT: LNG)

Sabine Pass LNG, L.P.

(“SPLNG”)

Sabine Pass

Liquefaction, LLC

(“SPL”)

Cheniere Energy

Partners, L.P.

(NYSE MKT: CQP)

Cheniere Creole Trail

Pipeline, L.P.

(“CTPL”)

Corpus Christi

Liquefaction, LLC

(“CCL”)

Cheniere

Marketing, LLC

(“CMI”)

Cheniere Energy

Partners GP, LLC

100% Interest

100% Interest

100% Interest

100% Interest

Note: This organizational chart is provided for illustrative purposes only, is not and does not purport to be a complete organizational chart of Cheniere.

(1) Current ownership interest based solely on ownership of Class B units. As Class B units accrete Blackstone will increase its ownership percentage, and the public and CQH will have reduced

ownership percentages.

(2) Cheniere Energy, Inc. has agreed in principle to partner with Parallax Enterprises, LLC on these projects.

Liquefaction facilities

9 mtpa under

construction

13.5 mtpa under

development

10.1 Bcf of storage

2 berths

Regasification facilities

4.0 Bcf/d of capacity

17.0 Bcf of storage

2 berths

Liquefaction facilities

22.5 mtpa under construction

4.5 mtpa under development

Cheniere Energy Partners

LP Holdings, LLC

(NYSE MKT: CQH)

1.5 Bcf/d capacity for SPL

Provides gas supply for SPL

80.1% Interest

55.9% Interest

(1)

2.0% Interest & Incentive

Dist. Rights

Int’l LNG marketing

SPAs with SPL and CCL

Three 5-year LNG vessel

charters

Blackstone (BX) 29.0%

(1)

Public 13.1%

(1)

Public

19.9%

22

Other Project

Developments

100% Interest

Agreement in

Principle for

Liquefaction

facilities at Live Oak

LNG and Louisiana

LNG

2

~10 mtpa under

development

Other hydrocarbon

export facilities

Cheniere’s Debt Summary

As of October 2015

Cheniere Energy, Inc.

(NYSE MKT: LNG)

Cheniere Energy Partners,

L.P. (NYSE MKT: CQP)

Sabine Pass LNG, L.P.

(SPLNG)

Total TUA (1 Bcf/d)

Chevron TUA (1 Bcf/d)

SPL TUA (2 Bcf/d)

Sr Secured Notes

$1,666 due 2016 (7.50%)

$420 due 2020 (6.50%)

($ in millions)

Cheniere Marketing, LLC

(CMI)

Trains 1-5 Debt

$4,600 Credit Facilities due 2020

1

$2,000 Notes due 2021 (5.625%)

$1,000 Notes due 2022 (6.250%)

$1,500 Notes due 2023 (5.625%)

$2,000 Notes due 2024 (5.750%)

$2,000 Notes due 2025 (5.625%)

$1,200 Working Capital Facility

due 2020

2

Sabine Pass

Liquefaction, LLC

(SPL)

Creole Trail Pipeline

(CTPL)

$400 Term Loan due 2017 (L+325)

CQP GP

(& IDRs)

(1) Includes $2,850 million term loan facility, $1,150 million Republic of Korea (“ROK”)

covered facility and $600 million ROK direct facility. Interest on the term loan facility is

L+175 bps during construction and operation. Under the ROK credit facilities, interest

includes L+175 on the direct portion and L+130 on the covered portion during

construction and operation. In addition, SPL will pay 45 bps for insurance/guarantee

premiums on any drawn amounts under the covered tranches. These credit facilities

mature on the earlier of December 31, 2020 or the second anniversary of Train 5

completion date.

(2) Interest on the working capital facility is L+175.

(3) Interest on the term loan facility is L+225 bps during construction and L+250 bps

during operation. This credit facility matures on the earlier of May 13, 2022 or the second

anniversary of project completion date .

Note: This organizational chart is provided for illustrative purposes only, is not and does

not purport to be a complete organizational chart of Cheniere.

Cheniere Energy Partners

LP Holdings, LLC

(NYSE MKT: CQH)

23

Cheniere CCH

Holdco II, LLC

Convertible Debt

$1,000 PIK Convertible Notes due 2021 (4.875%)

$625 Convertible Notes due 2045 (4.250%)

SPL Firm Transport (1.5 Bcf/d)

BG SPA (286.5 Tbtu / yr)

Gas Natural SPA (182.5 Tbtu / yr)

KOGAS SPA (182.5 Tbtu / yr)

GAIL (182.5 Tbtu / yr)

Total (104.8 Tbtu / yr)

Centrica (91.3 Tbtu / yr)

CMI SPA

Pertamina SPA (79.4 Tbtu / yr)

Endesa SPA (117.3 Tbtu / yr)

Iberdrola SPA (39.7 Tbtu / yr)

Gas Natural (78.2 Tbtu / yr)

Woodside (44.1 Tbtu / yr)

EDF (40.0 Tbtu / yr)

EDP (40.0 Tbtu / yr)

CMI SPA

Cheniere Corpus Christi

Holdings, LLC

(CCH)

Trains 1-2 Equity

$1,000 Senior Secured

Convertible Notes due

2025

Trains 1-2 Debt

~$8,400 Credit Facility due

2022

3

Corpus Christi

Liquefaction, LLC

(CCL)

Conversion of Class B and Subordinated Units

Mandatory conversion: within 90 days of the substantial completion of Train 3

Optional conversion by a Class B unitholder may occur at any of the following times:

• After 83 months from issuance of EPC notice to proceed

• Prior to the record date for a quarter in which sufficient cash from operating surplus is

generated to distribute $0.425 to all outstanding common units and the common units to be

issued upon conversion

• Thirty (30) days prior to the mandatory conversion date

• Within a 30-day period prior to a significant event or a dissolution

Subordinated units will convert into common units on a one-for-one basis, provided that there

are no cumulative common unit arrearages, and either of the below distribution hurdles is met:

• For three consecutive, non-overlapping four-quarter periods, the distribution paid from

“Adjusted Operating Surplus”

(1)

to all outstanding units

(2)

equals or exceeds $0.425 per

quarter

• For four consecutive quarters, the distribution paid from “Contracted Adjusted Operating

Surplus”

(1)

to all outstanding units

(2)

equals or exceeds $0.638 per quarter

Class B Units:

Subordinated Units:

(1) As defined in CQP’s partnership agreement.

(2) Includes all outstanding common units (assuming conversion of all Class B units), subordinated units and any other outstanding units that are senior or equal in right of distribution to the

subordinated units.

24

Sabine Pass Liquefaction –– Brownfield LNG Export Project

Utilizes Existing Assets, Trains 1-5 Under Construction

Significant infrastructure in place including storage, marine and pipeline interconnection facilities;

pipeline quality natural gas to be sourced from U.S. pipeline network

Design production capacity is expected to be ~4.5 mtpa per train, using ConocoPhillips’

Optimized Cascade® Process

Current Facility

~1,000 acres in Cameron Parish, LA

40 ft. ship channel 3.7 miles from coast

2 berths; 4 dedicated tugs

5 LNG storage tanks (~17 Bcfe of storage)

5.3 Bcf/d of pipeline interconnection

Liquefaction Trains 1 – 5: Fully Contracted

Lump Sum Turnkey EPC contracts w/ Bechtel

T1 & T2 EPC contract price ~$4.1B

• Overall project ~96% complete (as of 10/2015)

• Operations estimated late 2015/2016

T3 & T4 EPC contract price ~$3.8B

• Overall project ~77% complete (as of 10/2015)

• Operations estimated 2016/2017

T5 EPC contract price ~$3.0B

• Construction commenced June 2015

Liquefaction Train 6

FID upon obtaining commercial contracts

and financing

Artist’s rendition

25

SPL estimated cash flows

($ in billions)

SPL Trains 1-5 SPL Trains 1-6

Long term SPAs $2.9 $3.2

CMI SPA payment

(1)

$0.4 $0.9

Commodity payments, net

(2)

$0.3 $0.4

Total SPL revenues $3.6 $4.4

SPLNG TUA payments

(3)

($0.4) ($0.4)

Plant O&M ($0.3) ($0.3)

Plant maintenance capex

(4)

($0.2) ($0.2)

Pipeline costs (primary plant and upstream pipelines) ($0.2) ($0.2)

Total SPL operating expenses ($1.1) ($1.2)

SPL EBITDA $2.6 $3.3

Less: Project-level interest expense

(5)

($0.8) ($0.9)

SPL distributable cash flow to CQP $1.8 $2.3

SPL Estimated Cash Flows

Trains 1-5 and Trains 1-6

26

Note: EBITDA is a non-GAAP measure. EBITDA is computed as total revenues less non-cash deferred revenues, operating expenses, assumed commissioning costs and state and local taxes. It does

not include depreciation expenses and certain non-operating items. Because we have not forecasted depreciation expense and non-operating items, we have not made any forecast of net

income, which would be the most directly comparable financial measure under generally accepted accounting principles, or GAAP, and we are unable to reconcile differences between

forecasts of EBITDA and net income. EBITDA has limitations as an analytical tool and should not be considered in isolation or in lieu of an analysis of our results as reported under GAAP, and

should be evaluated only on a supplementary basis.

Assumes future long term contracting of additional 1.5 MTPA at SPL Train 6 (total of 21.25 MTPA of long term SPAs at SPL Trains 1-6) at $3.50 per MMBtu.

(1) CMI SPA payment assumes 100% utilization at $3.00/MMBtu.

(2) Assumes $5.00/MMBtu natural gas price and that off-takers lift 100% of their full contractual entitlement. Amounts are net of estimated natural gas to be used for the liquefaction process.

(3) Includes payments related to reassignment of Total TUA SPLNG capacity and export fees paid to SPLNG.

(4) Majority of costs shown are fixed and covered under multi-year service and supply agreements with equipment and service providers.

(5) Assumes debt at SPL refinanced at 6.00% annual interest rate.

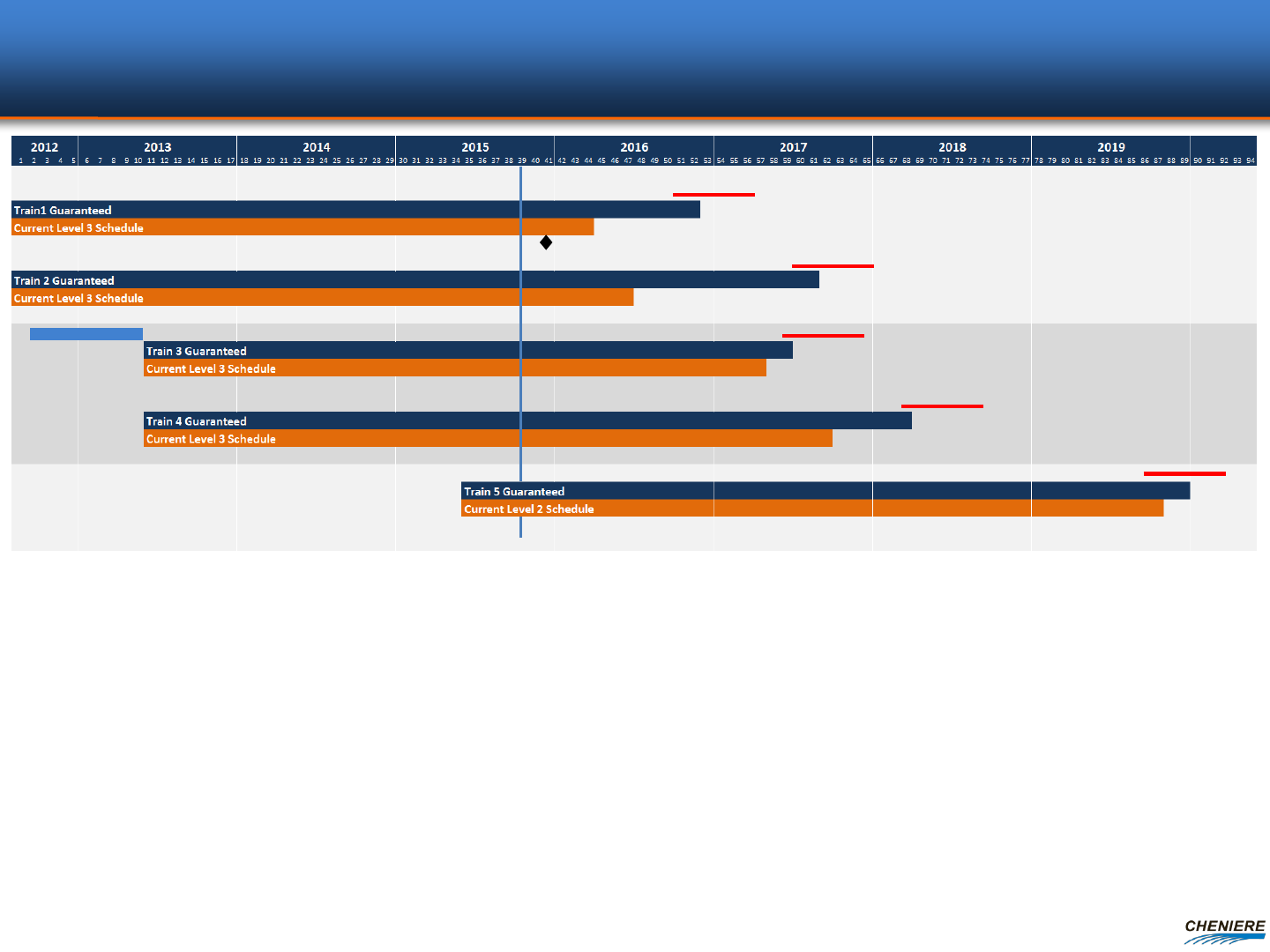

SPL Construction Completion Schedules Trains 1 – 5

Stage 1 (Trains 1&2) overall project progress as of October 2015 is 96.1% complete vs. Target Plan of 98.2%:

Engineering, Procurement, Subcontracts and Construction are 100%, 100%, 84.1% and 93.5% complete against Target Plan of 99.8%,

100%, 88.7% and 98.1% respectively

Bechtel Delivered the Train 1 Commissioning and Start-up Plan in Feb, projecting Fuel Gas introduction in Sep, Feed Gas introduction in

Oct, and Ready for Start-up in Dec; all in support of the current First LNG Target

by year-end 2015, and Target Substantial Completion in Mar 2016

Stage 2 (Trains 3&4) overall project progress as of October 2015 is 76.7% complete vs. Target Plan of 81.8%:

Engineering, Procurement, Subcontracts and Construction are 100%, 99.4%, 50.4% and 48.5% complete against Target Plan of 99.0%,

98.8%, 65.8% and 59.6% respectively

Stage 3 (Trains 5&6) overall project progress:

NTP on Train 5 issued to Bechtel on June 30

th

Soil stabilization civil works are in progress and the current plan estimates Train 5 operational in 52 months from NTP

BG DFCD

GN DFCD

KOGAS DFCD

GAIL DFCD

First LNG

March 2016

April 2017

Jun 2017

Mar 2018

June 2016

Sept 2017

27

Dec 2019

Oct 2019

Early Engineering

TOTAL & CENTRICA DFCD

LNG Sale and Purchase Agreements (SPAs)

Sabine Pass Liquefaction

(1) BG has agreed to purchase 182,500,000 MMBtu, 36,500,000 MMBtu, 34,000,000 MMBtu and 33,500,000 MMBtu of LNG volumes annually upon the commencement of operations of Trains 1, 2, 3 and 4,

respectively. Total has agreed to purchase 91,250,000 MMBtu of LNG volumes annually plus 13,400,000 MMBtu of seasonal LNG volumes upon the commencement of Train 5 operations.

(2) A portion of the fee is subject to inflation, approximately 15% for BG Group, 13.6% for Gas Natural Fenosa, 11.5% for KOGAS, GAIL (India) Ltd, Total and Centrica.

(3) Following commercial in service date of Train 4. BG will provide annual fixed fees of approximately $520 million during Trains 1-2 operations and an additional $203 million once Trains 3-4 are operational.

(4) SPAs have a 20 year term with the right to extend up to an additional 10 years. Gas Natural Fenosa has an extension right up to an additional 12 years in certain circumstances.

(5) Ratings are provided by S&P/Moody’s/Fitch and subject to change, suspension or withdrawal at anytime and are not a recommendation to buy, hold or sell any security.

BG Gulf Coast LNG

Gas Natural Fenosa

Annual Contract

Quantity (MMBtu)

286,500,000

(1)

Fixed Fees $/MMBtu

(2)

Annual Fixed Fees

(2)

~$723 MM

(3)

~$454 MM

Term of Contract

(4)

Guarantor

20 years

BG Energy

Holdings Ltd.

Gas Natural

SDG S.A.

Corporate / Guarantor

Credit Rating

(5)

A-/A2/A- BBB/Baa2/BBB+

Fee During Force

Majeure

Up to 24 months

Up to 24 months

20 years

GAIL (India) Limited

~$548 MM

20 years

NR/Baa2/BBB-

N/A

N/A

Contract Start

Train 1 + additional

volumes with Trains 2,3,4

Train 2

Train 4

$2.25 - $3.00 $2.49

$3.00

182,500,000

182,500,000

20 years

N/A

N/A

A+/Aa3/AA-

Train 3

$3.00

~$548 MM

Korea Gas Corporation

182,500,000

~$314 MM

20 years

AA-/Aa1/AA-

N/A

Total S.A.

Train 5

$3.00

104,750,000

(1)

Total Gas & Power N.A.

~$274 MM

20 years

BBB+/Baa1/A-

N/A

N/A

$3.00

91,250,000

Centrica plc

Train 5

LNG Cost

115% of HH

115% of HH

115% of HH

115% of HH

115% of HH

115% of HH

~20 mtpa “take-or-pay” style commercial agreements

~$2.9B annual fixed fee revenue for 20 years

28

Corpus Christi Liquefaction Project

29

Proposed 5 Train Facility

>1,000 acres owned and/or controlled

2 berths, 4 LNG storage tanks (~13.5 Bcfe of storage)

Key Project Attributes

45 ft. ship channel 14 miles from coast

Protected berth

Premier Site Conditions

23-mile 48” and 42” parallel pipelines will connect to

several interstate and intrastate pipelines

Liquefaction Trains 1-2: Under Construction

Lump Sum Turnkey EPC contracts w/ Bechtel

T1 & T2 EPC contract price ~$7.1B

• Construction commenced May 2015

• Operations estimated 2018

Liquefaction Train 3: Partially Contracted

0.8 mtpa contracted to date

Targeting additional 2.1 mtpa

Reach FID upon contracting

Liquefaction Trains 4-5: Initiated Development

Permit process started June 2015

Houston

New Orleans

Gulf of Mexico

Corpus Christi

Commenced Construction on Trains 1-2 in May 2015

Artist’s rendition

Design production capacity is expected to be ~4.5 mtpa per train,

using ConocoPhillips’ Optimized Cascade® Process

Under

Construction

Trains 1-2

Train 3

Initiated

Development

Trains 4-5

CCL estimated cash flows

($ in billions)

CCL Trains 1-2 CCL Trains 1-3

Long term SPAs $1.4 $1.9

CMI SPA payment

(1)

$0.2 $0.5

Commodity payments, net

(2)

$0.1 $0.1

Total CCL revenues $1.7 $2.5

Plant O&M ($0.2) ($0.2)

Plant maintenance capex

(3)

($0.1) ($0.1)

Pipeline costs (primary plant and upstream pipelines) ($0.1) ($0.2)

Total CCL operating expenses ($0.4) ($0.5)

CCL EBITDA $1.3 $2.0

Less: Project-level interest expense

(4)

($0.5) ($0.7)

CCL distributable cash flow to CEI $0.8 $1.3

CCL Estimated Cash Flows

Trains 1-2 and Trains 1-3

30

Note: EBITDA is a non-GAAP measure. EBITDA is computed as total revenues less non-cash deferred revenues, operating expenses, assumed commissioning costs and state and local taxes. It does

not include depreciation expenses and certain non-operating items. Because we have not forecasted depreciation expense and non-operating items, we have not made any forecast of net

income, which would be the most directly comparable financial measure under generally accepted accounting principles, or GAAP, and we are unable to reconcile differences between

forecasts of EBITDA and net income. EBITDA has limitations as an analytical tool and should not be considered in isolation or in lieu of an analysis of our results as reported under GAAP, and

should be evaluated only on a supplementary basis.

Assumes future long term contracting of additional ~2.1 MTPA at CCL Train 3 (total of 10.5 MTPA of long term SPAs at CCL Trains 1-3) at $3.50 per MMBtu.

(1) CMI SPA payment assumes 100% utilization at $3.00/MMBtu.

(2) Assumes $5.00/MMBtu natural gas price and that off-takers lift 100% of their full contractual entitlement. Amounts are net of estimated natural gas to be used for the liquefaction process.

(3) Majority of costs shown related to service-based payments to be contracted over a multi-year term.

(4) Assumes debt at CCL refinanced at 6.00% annual interest rate.

Corpus Christi Liquefaction Project Schedule

Stage 1 (Trains 1&2) overall project progress as of October 2015 is ahead of target:

Engineering, Procurement, and Construction has progressed to 90.3%, 34.6%, and 0.8%

compared to a plan of 82.3%, 23.0%, and 1.7% respectively.

NTP issued, construction commenced for Trains 1-2 in May 2015

31

Note: Based on Guaranteed Substantial and Target Completion Dates per EPC contract.

Train 1 Guaranteed

Current Level 3 Schedule

Train 2 Guaranteed

Current Level 3 Schedule

Train 1 DFCD

Train 2 DFCD

Oct-19

Feb-19

Jul-20

Jun-19

PT Pertamina

(Persero)

Endesa S.A.

Iberdrola S.A.

Gas Natural Fenosa

Woodside Energy

Trading

Électricité de

France

EDP Energias de

Portugal S.A.

Annual Contract

Quantity (TBtu)

79.36 117.32 39.68 78.20 44.12 40.00 40.00

Annual Fixed Fees

(1)

~$278 MM ~$411 MM ~$139 MM ~$274 MM ~$154 MM ~$140 MM ~$140 MM

Fixed Fees $/MMBtu

(1)

$3.50 $3.50 $3.50 $3.50 $3.50 $3.50 $3.50

LNG Cost

115% of HH 115% of HH 115% of HH 115% of HH 115% of HH 115% of HH 115% of HH

Term of Contract

(2)

20 years 20 years 20 years 20 years 20 years 20 years 20 years

Guarantor

N/A N/A N/A

Gas Natural

SDG, S.A.

Woodside

Petroleum, LTD

N/A N/A

Guarantor/Corporate

Credit Rating

(3)

BB+/Baa3/BBB- BBB/Baa2/BBB+ BBB/Baa1/BBB+ BBB/Baa2/BBB+ BBB+/Baa1/BBB+

A+/A1/A BB+/Baa3/BBB-

Contract Start

Train 1 / Train2

Train 1

Train 1 / Train 2

Train 2

Train 2

Train 2

Train 3

Corpus Christi Liquefaction SPAs

SPA progress: ~8.42 mtpa “take-or-pay” style commercial agreements

~$1.5B annual fixed fee revenue for 20 years

(1) 12.75% of the fee is subject to inflation for Pertamina; 11.5% for Woodside; 14% for all others

(2) SPA has a 20 year term with the right to extend up to an additional 10 years.

(3) Ratings are provided by S&P/Moody’s/Fitch and subject to change, suspension or withdrawal at anytime and are not a recommendation to buy, hold or sell any security.

32

Live Oak and Louisiana Liquefaction Projects

1

33

Live Oak LNG Facility Overview

340 acres on the Calcasieu Channel,

just north of Calcasieu Lake

~5 mtpa development

1 berth, 2 LNG storage tanks

Project Update

FERC pre-filing expected in 2015

First LNG expected 2021

Louisiana LNG Facility Overview

400 acres on the Mississippi River,

~40 miles downstream from the

Port of New Orleans

~5 mtpa development

1 berth, 2 LNG storage tanks

Project Update

FERC pre-filing for 6 mtpa in July 2015

First LNG expected 2021

Artist’s rendition for both projects

Mid-scale LNG projects Utilizing Bechtel/Chart Industries Technology

Live Oak

LNG

Louisiana

LNG

(1) Cheniere Energy, Inc. has agreed in principle to partner with Parallax Enterprises, LLC on these projects

Applications Filed with FERC for Liquefaction Projects

Continental U.S.

LNG Export Projects

Quantity

Bcf/d

FERC

Pre-filing

Date

FERC

Application

Date

FERC

Scheduling

Notice Issued

EIS /

EA

Scheduled

Date for EIS

or EA

FERC Approval

DOE

Non FTA

Final

Under

Construction

Sabine Pass Liquefaction T1-4 2.8 7/26/10 1/31/11 12/16/11 EA 4/16/12 8/7/12

Cameron LNG T1-3 1.7 4/30/12 12/10/12 11/21/13 EIS 4/30/14 6/19/14 9/10/14

Freeport LNG

1.4

0.4

12/23/10 8/31/12 1/6/14 EIS 6/16/14 7/30/14 11/14/14

Dominion Cove Point LNG 1.0 6/1/12 4/1/13 3/12/14 EA 5/15/14 9/29/14 5/7/15

Corpus Christi Liquefaction T1-3 2.1 12/13/11 8/31/12 2/12/14 EIS 10/8/14 12/30/14 5/12/15

T1-2:

Sabine Pass Liquefaction T5-6 1.38 2/27/13 9/30/13 11/03/14 EA 12/12/14 4/6/2015

6/26/15

T5:

Jordan Cove Energy 1.2/0.8 2/29/12 5/22/13 7/16/14 EIS 9/30/15

Oregon LNG 1.25 7/3/12 6/7/13 4/17/15 EIS 2/12/16

Lake Charles LNG 2.0 3/30/12 3/25/14 1/26/15 EIS 8/14/15

Magnolia 1.08 3/20/13 4/30/14 4/30/15 EIS 11/16/15

Southern LNG 0.5 12/5/12 3/10/14 EA

Golden Pass 2.6 5/16/13 7/7/14 6/26/15 EA 3/4/16

Gulf LNG 1.3 12/6/12 6/19/15 EIS

Cameron LNG Expansion T4-5 1.4 2/24/15 9/28/15 EIS

Note: National Environmental Policy Act (NEPA) empowers FERC as the lead Federal agency to prepare an Environmental Impact Statement in cooperation with other state and federal agencies

Source: Office of Fossil Energy, U.S. Department of Energy; U.S. Federal Energy Regulatory Commission; Company releases

6 projects have received FERC approval and final DOE approval for Non FTA

34

Source: Office of Oil and Gas Global Security and Supply, Office of Fossil Energy, U.S. Department of Energy;

U.S. Federal Energy Regulatory Commission; Company releases

U.S. LNG Export Projects

Dominion Cove Point

Under Construction

Company

Quantity

(Bcf/d)

DOE FERC Contracts

Cheniere Sabine

Pass T1 – T4

2.2

Fully permitted

Fully

Subscribed

Freeport

1.8

Fully permitted

Fully

Subscribed

Lake Charles

2.0

FTA +

NonFTA

Fully

Subscribed

Dominion Cove

Point

1.0

Fully permitted

Fully

Subscribed

Cameron LNG T1-3

1.7

Fully permitted

Fully

Subscribed

Jordan Cove

1.2/0.8

FTA +

NonFTA

Oregon LNG

1.25

FTA +

NonFTA

Cheniere Corpus

Christi T1 – T3

2.1

Fully permitted

Partially

Subscribed

Cheniere Sabine

Pass T5 – T6

1.3

Fully permitted

T5

Subscribed

Southern LNG

0.5 FTA

v

Fully

Subscribed

Magnolia LNG

0.5 FTA

Partially

Subscribed

Golden Pass LNG

2 FTA

Fully

Subscribed

Gulf LNG

1.3 FTA

v

Cameron LNG T4-5

1.4 FTA

v

Freeport LNG

Corpus Christi

Plus other proposed LNG export projects that have not filed a FERC application.

Excelerate has requested that FERC put on hold the review its application.

• Application filing = v

• FERC scheduling notice issued =

Filed FERC Application

Jordan Cove

Oregon LNG

Cameron LNG

Lake Charles

Sabine Pass

35

Southern LNG

Gulf LNG

Golden Pass

Magnolia

{kind=link}