THE BALANCED SCORECARD AND

TABLEAU DE BORD:

A

GLOBAL PERSPECTIVE ON TRANSLATING

STRATEGY INTO ACTION

by

M. J.

EPSTEIN*

and

J. F.

MANZONI**

97/63/AC/SM

Price Waterhouse Visiting Professor of Accounting and Control at INSEAD, Boulevard de Constance,

77305 Fontainebleau Cedex, France.

Assistant Professor of Accounting and Control at INSEAD, Boulevard de Constance, 77305

Fontainebleau Cedex, France.

A working paper in the INSEAD Working Paper Series is intended as a means whereby a faculty researcher's

thoughts and findings may be communicated to interested readers. The paper should be considered preliminary

in nature and may require revision.

This version of the paper is intended for a practitioner audience.

Printed at INSEAD, Fontainebleau, France.

The Balanced Scorecard and Tableau de Bord: A Global Perspective on

Translating Strategy into Action

by Marc J. Epstein and Jean-Francois Manzoni

INSEAD, The European Institute of Business Administration, Bd. de Constance, F-77300 Fontainebleau, France

(P) 33 1 6072 40 00 (F) 33 1 64 22 77 31 (E) epstein@inseadfr or manzoni@inseadfr

Abstract

Over twenty years ago Steven Kerr wrote an article entitled "On the folly of hoping for A

and rewarding B". The paper, now considered a "classic", described how many

companies' performance measurement systems were rewarding different behaviors than

the ones they hoped to obtain from their employees. This issue has received much

attention over the last few years. In particular, Robert Kaplan and David Norton have

published a series of three Harvard Business Review articles proposing a specific

framework, called Balanced Scorecard, to facilitate the translation of strategy into action.

The idea of having some form of balanced picture of company performance is not new in

itself. Many companies have for years tracked and reported multiple indicators. Further,

many countries have also had particular traditions. In France, for example, companies

have been using a related tool called "Tableau de Bord" for over fifty years. The paper

reviews and compares Tableau de Bord and Balanced Scorecard. We conclude that

Kaplan and Norton's Balanced Scorecard represents a welcome addition and goes

further than what most companies and countries were doing.

For years, companies have found that achievement of long term goals typically

requires clearly focused corporate and functional strategies. James Collins and Jerry

Porras, for example, found in their best selling book

Built to Last,

that companies that

have a clear understanding of who they are and what they are trying to achieve also

enjoy the greatest long-term success. This issue has been around for a long time.

Over twenty years ago Steven Kerr wrote an article that summarized many

companies' practices in "On the folly of rewarding A, while hoping for B".

1

The

article described how many companies' performance measurement systems were

rewarding different behaviors than the ones they hoped to obtain from their

employees.

This concern has been echoed in the accounting literature; over the last few years,

Management Accounting and other publications have published numerous articles

emphasizing three key points:

•

Companies should establish performance measurement systems that

support their strategies

•

Performance measurement systems should contain many non-financial

indicators to complement financial ones, particularly with respect to customer

perceptions and performance of internal processes.

•

The company's overall performance measurement system should then be

broken down into sets of local measurements for lower-level units, to translate

(cascade) the firm's objectives into more actionable sub-sets.

Five years ago, in the first of three Harvard Business Review articles on the

subject, Robert Kaplan and David Norton proposed a specific framework, called

'Steven Kerr, "On the Folly of Rewarding A, while Hoping for B",

Academy of Management Journal

(1975, pp. 769-783).

2

Balanced Scorecard, to facilitate the translation of strategy into action.

2

The

Balanced Scorecard is a short document summarizing succinctly a set of leading and

lagging performance indicators grouped into four different perspectives: financial,

customer, internal processes, and learning and growth (see Figure 1).

The idea of having some form of balanced picture of company performance is not

new in itself. Many companies have for years tracked and reported multiple

indicators. Further, many countries have also had particular traditions. In France,

for example, companies have been using a related tool called "Tableau de Bord" for

over fifty years. Still, Kaplan and Norton's Balanced Scorecard represents a welcome

addition and goes further than what most companies and countries were doing.

Tableau de Bord in France

A Tableau de Bord is a "dashboard", such as the one on which plane pilots and car

drivers can observe the speed at which they are going, how many miles they have

covered so far, and how much fuel they are consuming. The Tableau de Bord

emerged in France at the turn of this century. It was first developed by process

engineers who were looking for ways to improve their production process by better

understanding cause-effect relationships (the relationships between actions and

process performance). The same principle was then applied at the top management

level, to give senior managers a set of indicators allowing them to monitor the

progress of the business, compare it to the goals that had been set, and take

corrective actions.

This initial objective, giving managers a succinct overview of key parameters to

support decision making, had two important implications: First, the Tableau de Bord

cannot be a single document applying equally well to the whole firm; because each

sub-unit, and in fact each manager, has different responsibilities and objectives, there

2

See "The Balanced Scorecard - Measures that Drive Performance" (Harvard Business Review,

January-February 1992), "Putting the Balanced Scorecard to Work" (HBR, September-October 1993),

and "Using the Balanced Scorecard

as a

Strategic Management System" (HBR, January-February

1996). Kaplan and Norton recently expanded on their ideas in a book called

The Balanced Scorecard:

Translating Strategy into Action

(Harvard Business School Press, 1996).

3

should be one Tableau de Bord for each sub-unit. These "dashboards" should be

integrated in a nested structure, like the one illustrated by a set of Russian dolls. In

this context, the firm's overall Tableau de Bord would translate into a series of

documents supporting local decision making.

Secondly, the various Tableaux de Bord used within the firm should not be limited to

financial indicators. Operational measures often give better information on the

impact of "local" events and decisions, and thus on cause-effect relationships, than

overall financial indicators.

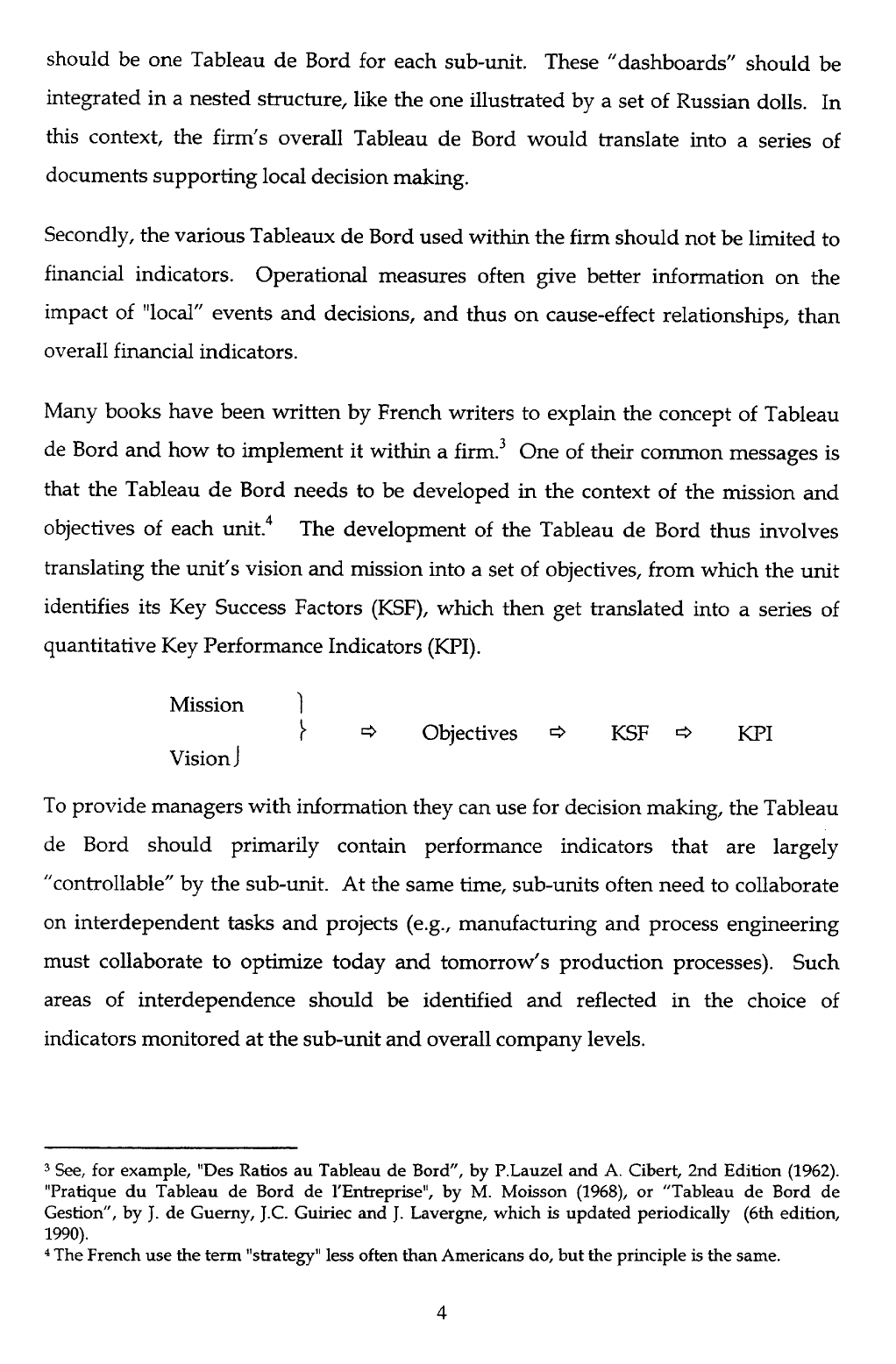

Many books have been written by French writers to explain the concept of Tableau

de Bord and how to implement it within a firm.

3

One of their common messages is

that the Tableau de Bord needs to be developed in the context of the mission and

objectives of each unit.

4

The development of the Tableau de Bord thus involves

translating the unit's vision and mission into a set of objectives, from which the unit

identifies its Key Success Factors (KSF), which then get translated into a series of

quantitative Key Performance Indicators (KPI).

Mission

1

=>

Objectives

12

?

KSF =>

KPI

Vision i

To provide managers with information they can use for decision making, the Tableau

de Bord should primarily contain performance indicators that are largely

"controllable" by the sub-unit. At the same time, sub-units often need to collaborate

on interdependent tasks and projects (e.g., manufacturing and process engineering

must collaborate to optimize today and tomorrow's production processes). Such

areas of interdependence should be identified and reflected in the choice of

indicators monitored at the sub-unit and overall company levels.

3

See, for example, "Des Ratios au Tableau de Bord", by P.Lauzel and A. Cibert, 2nd Edition (1962).

"Pratique du Tableau de Bord de l'Entreprise", by M. Moisson (1968), or "Tableau de Bord de

Gestion", by J. de Guerny, J.C. Guiriec and J. Lavergne, which is updated periodically (6th edition,

1990).

4

The French use the term "strategy" less often than Americans do, but the principle is the same.

4

Concretely, the Tableau de Bord document should report actual performance of the

(sub-)unit on a small number of indicators; conciseness is important and the danger

of overloading managers with information is often highlighted by French authors.

The report should include numbers covering the period since the last report, and

may also present cumulative performance since the beginning of the year. Actual

performance should be compared to some yardstick chosen on the basis of both past

performance and external benchmarking.

5

The periodicity of the report should be a

function of the unit's responsibilities and the nature of the data, but a monthly

revision is considered typical at the top management level.

More than a mere document, French writers position the Tableau de Bord within an

"overall management approach". Aside from the document itself, which is useful in

its own right to support local decision making, a firm can derive much value from:

•

The

Tableau de Bord development process,

which forces each unit, function or

division to identify its objectives and Key Success Factors, and the areas of

interdependence with other sub-units,

•

The

discussions

that will be triggered by the publication of the Tableau de

Bord, which will provide opportunities for learning throughout the firm and for

reinforcing the firm's overall mission.

Overall, the Tableau de Bord document and the processes in which it is embedded

could thus yield four types of benefits.

1.

Provide each manager with a periodic succinct overview of the performance

of its unit to guide decision making.

2.

Inform the next level up of the sub-unit's performance (a complement to

decentralization of responsibilities).

5

This emphasis on benchmarking with other firms already appeared in the 1962 textbook on Tableaux

de Bord.

5

3.

Force each sub-unit to (a) position itself within the context of the firm's overall

strategy and the responsibilities of other sub-units, and (b) identify corresponding

KSF and KPI.

4.

The company's overall Tableau de Bord and its sub-unit applications

contribute to structuring management's agenda and directing managerial focus and

discussions.

The concept of Balanced Scorecard

The concept of balanced scorecard came out of the realization that no single

performance indicator can capture the full complexity of an organization's

performance. In particular, financial indicators have well-known weaknesses, such

as capturing the impact of decisions with a significant time lag. As a result they tend

to be less proactive indicators of potential problems than operational (non-financial)

indicators. Many articles published in the 1980s following the TQM movement

emphasized the need to complement financial indicators with non-financial ones.

Several articles went in fact a step further and recommended reducing the focus on

financial indicators, which were said to encourage managers to make decisions that

were not in the best interests of the company.

We now know that financial and non-financial indicators should not be viewed as

substitutes. While financial measures tend to be lagging indicators of performance

(they tend to capture the impact of decisions only when their financial consequences

materialize, which can be long after the decision was made), they also have two

important benefits: (1) They represent the impact of decisions in a comparable

measurement unit -money, which allows aggregation of results across units, and (2)

they capture the cost of trade-offs between resources as well as the cost of spare

capacity. Business organizations exist in large part to create value for shareholders;

financial performance thus remains an essential parameter. Ultimately,

improvement on non-financial measures should translate into superior financial

performance.

6

While several organizations were tracking and reporting many non-financial

indicators, Kaplan and Norton went one step further by proposing a framework,

called Balanced Scorecard, that has three important characteristics:

•

it presents

on a single document,

a series of indicators providing a more

complete view of the company's performance;

•

this document is supposed to be short and connected to the company's

information system for further detail (rather than the monthly "book" that many

organizations still produce and which requires enormous managerial time and skill

to digest);

•

instead of listing indicators in an ad hoc manner, the Balanced Scorecard

groups the indicators into four "boxes", each capturing a distinct perspective on the

company's performance but all linked to its vision and strategy (see Figure 1).

The financial perspective focuses on the shareholders' interests: is the company

generating satisfactory return on investment and creating shareholder value? The

three other perspectives can be explained through the following reasoning: How

does a company succeed financially? Through a combination of two elements: One

is creating value for customers; we thus need to know how customers perceive our

performance. But a firm can delight customers all the way into bankruptcy, so it also

need to make sure that it performs well on key internal dimensions. For example, we

can improve customer service by having massive numbers of employees servicing

customers, or by having less employees whose time we utilize more efficiently and

whom we support with excellent information technology. Creating value for

customers only translates into shareholder value if it is based on effective and

efficient key internal processes.

The next step is to make this value creation sustainable over time. The company may

create value for customers and make excellent use of its resources

today,

but the

world does not stand still and performance requirements keep ratcheting up over

time. To make sure that the company will still be appreciated by tomorrow's

7

customers and will keep making excellent use of its resources, the organization and

its employees must keep learning and developing. This perspective should thus

group indicators capturing the company's performance with respect to innovation,

learning and growth.

From this reasoning comes a set of four perspectives, each characterized by a small

set of performance measures. As in the "Tableau de Bord", the specific content of

these four "boxes" must be adapted to the circumstances of each organization. In

particular, the four sets of indicators should reflect and operationalize the

organization's mission and strategy. A company following a low cost strategy will

have different Key Success Factors than one creating value through very innovative

products targeted at a subset of the overall market. These two organizations should

track different indicators to assess how well they are doing and guide performance

improvement programs.

Also similar to the Tableau de Bord, the concept of balanced scorecard can be

cascaded down through the organization to achieve a dual purpose: customization of

the balanced scorecard to the (sub-)unit by identifying its own set of actionable

performance indicators, and alignment of the sub-units within the company's overall

vision and strategy.

A Balanced Scorecard contains a set of performance metrics, some considered

"lagging indicators", others considered "leading indicators". In practice the notion

of leading vs. lagging indicator should really be thought of as a continuum.

Customer satisfaction, for example, is a leading indicator of financial performance,

but (assuming on-time-delivery is an important factor for the firm's customers) it is

also a lagging indicator of on-time-delivery. On-time-delivery is a leading indicator

of customer satisfaction, but it is determined in part by, and thus is a lagging

indicator of, production cycle time and quality of both product and process. It is in

fact possible to reflect such relationships between means and ends, or between causes

and effects, through the Balanced Scorecard (see Figure 2).

8

Main benefits of implementing a tool such as Balanced Scorecard or Tableau de

Bord

Developing and using a Balanced Scorecard or Tableau de Bord can bring several

benefits to a firm, some quite obvious, others more subtle. The most obvious

advantages are:

The Balanced Scorecard summarizes on a single, succinct document, four

different perspectives on the company's performance. Most organizations collect

some performance measures addressing some or all of these perspectives, but these

measures are typically reported in several different documents, often bulky, and

typically containing too much information to allow good analysis. Balanced

Scorecards and Tableaux de Bord group a small set of selected indicators on a single,

succinct document.

Because the four perspectives provide a more "balanced" view of the

company, they also allow managers to keep an eye on the way performance is

achieved (on the means used by managers). In particular, the Balanced Scorecard

highlights trade-offs between measures. A liquor company we worked with was in

the habit of pushing sales to distributors during the last week of each period, thus

overloading the distribution pipe line and "borrowing" sales from the next period.

Everybody knew that the practice was commonly used, but no one (but the people

close to the operations) knew exactly the amounts involved. In a Balanced Scorecard

context, such practices could easily be spotted through various measures focused on

customer satisfaction and number of weeks of distributor inventory.

Beyond these obvious benefits, the Balanced Scorecard is also a way for the company

to communicate and reinforce its strategy through its ranks. The presence of a

Balanced Scorecard does not eliminate the need for top managers to explain what

they are trying to achieve and why, but it

reinforces

traditional means of

communication by translating the strategy into quantifiable indicators. The firm's

Balanced Scorecard, in turn, can be translated into "local" scorecards for lower level

9

units, thus "cascading" the strategy and creating a set of "nested" performance

management systems.

Of course, tools like Balanced Scorecard and Tableau de Bord will have little impact

if they are never discussed. Rather than being used as a part of management-by-

exception, where indicators are only discussed if they fail to reach some pre-set

standard, the Balanced Scorecard should be part of a form of "interactive control"

and involve frequent and regular attention from operating managers through face-

to-face meetings of superiors, subordinates and peers. Rather than discussing

numbers for numbers' sake, discussions should be used to challenge and debate the

underlying data, assumptions and action plans. Unlike management-by-exception,

interactive control is not limited to unfavorable variances, it is systematic; we always

discuss where we stand on this metric.6

In this context, quantitative data are used not as an end in themselves but rather as a

mean

to

understand

and improve

the underlying

activities.

The Balanced Scorecard

then contributes to learning by structuring the agenda for meetings and discussions.

Such discussions can occur when reviewing the unit's performance for the month (or

the quarter), but also when evaluating new investments (how does this investment

impact the four perspectives presented on our scorecard), in the planning and

budgeting cycle, etc.

Finally, many companies have derived benefits from the very process of developing

a Balanced Scorecard. Just like many companies learn a lot about their activities and

processes from implementing Activity-Based-Costing, many firms realized while

developing a Balanced Scorecard that they did not really have clear views on the

strategy they were pursuing, nor on the key success factors of this strategy! In some

cases, senior management realized that they could not articulate a clear strategy. In

other cases, the problem was the opposite: too many people were articulating

different views on what the strategy of the firm really was! In both sets of cases,

6

For more on the notion of interactive vs. diagnostic control, see "Control in an Age of Empowerment",

by Robert Simons,

Harvard Business Review

(March-Apri11995).

10

development of the Balanced Scorecard forced the top management team to sit down

and develop a clear and shared view on what they were trying to achieve.

Did the French Tableau de Bord have it all?

As the previous sections make clear, the French notion of Tableau de Bord is quite

close to Kaplan and Norton's Balanced Scorecard from a conceptual point of view.

In practice, however, French Tableaux de Bord tend to fall significantly short of

Kaplan and Norton's Balanced Scorecard.

•

First, the French Tableaux de Bord we have observed tend to over-

emphasize financial measures and to contain much less non-financial measures than

books on Tableaux de Bord recommend. A comparative study of French and

American companies published shortly after Kaplan and Norton's first Balanced

Scorecard article reported similar findings.'

•

Also contrary to written advice, many companies chose goals and targets

that were mostly internal, with comparisons to last year's performance or this year's

budget, as opposed to systematic benchmarking of best-in-class performers.

•

Writings on the French Tableau de Bord go back more than forty years and

often fail to highlight important notions that we have learned over the last few years.

In particular, measures described in books on Tableau de Bord tend to be gathered

internally inside the firm, rather than externally from customers. French writers also

tend to refer to the company's or the sub-units' "mission and objectives", rather than

refer explicitly to their "strategy" as we would be more likely to do today.

•

Finally, with respect to the way the Tableau de Bord was used, French

managers seem to have often fallen into the trap of using the Tableau de Bord as a

device supporting management-from-a-distance and management-by-exception,

7

The study was conducted by two academics, one American and the other French. Their findings

were reported in the journal of the French association of accountants (Recent evolution of the Tableau

de Bord systems: comparison of practices in a few American and French multinationals, Jack Gray and

Yvon Pesqueux,

Revue Frangaise de Comptabilite,

February 1993).

11

rather than using it interactively to create an agenda for discussions and meetings.

As a result the Tableau de Bord lost much of its power and usefulness.

There are indications that French Tableaux de Bord are improving rapidly; several

recent articles in French business magazines report that an increasing number of

companies are collecting and reporting non-financial indicators, particularly external

data on customer perception. The increasing use of integrated computer systems

such as SAP and Oracle is also helping firms to collect, process and integrate data

that goes beyond "traditional" accounting measures. Still, it is fair to say that, at

least at the top management level, the content and style of use of French companies'

Tableaux de Bord often fell short of the theory on the subject.

Grouping indicators into "perspectives"

Some French authors point out that the notion of Tableau de Bord is wider and more

general than Kaplan and Norton's Balanced Scorecard, which they regard as a

"special case" of Tableau de Bord. These authors base their argument on the fact that

texts on the Tableau de Bord strongly emphasize the need to tailor-make the Tableau

de Bord to each company and to each manager within the company. As a result,

writings on the French Tableau de Bord generally do not specify structured sets of

indicators, while Kaplan and Norton's Balanced Scorecard proposes four generic sets

of indicators . The Balanced Scorecard approach can thus look more rigid and be

faulted by some as disregarding potentially important dimensions of firm

performance. For example, companies might want to highlight the following

dimensions by creating a specific "box" of indicators for them:

•

Impact of the firm on society

•

The firm's economic, political

and social environment

•

Consumers vs. customers

•

Major

projects

currently

underway

12

Firm's impact on employment, local

communities and environment; firm's record

on health and safety.

For firms selling through distributors and

which have two levels of constituencies: their

immediate customers and the final consumers.

price of raw materials, performance of the

overall industry, etc.)

Key milestones for the firm's major projects (to

ensure that progress on these projects -an

important leading indicator of future

performance- receives as much attention as

necessary.

Environmental contingencies that can have a

major impact on the firm's performance (e.g.,

In all fairness, however, this is not really a limitation of the Balanced Scorecard

model. First, some of the indicators addressing the "other" dimensions can often be

included in the four boxes proposed in the framework. Secondly, Kaplan and

Norton's four boxes are presented as an organizing framework rather than a

constraining straight-jacket. Nothing prevents companies from adding one or two

additional boxes, although part of the power of the Balanced Scorecard comes from

its conciseness and the clarity of its presentation; it is thus probably better to try to

keep the number of boxes rather small.

Finally, having a framework helps protect potential users against two dangers: the

danger of one particular perspective, for example the financial perspective, coming

to dominate the other perspectives by default (as has happened in many French

companies), and the danger of missing one of the four dimensions proposed in the

Balanced Scorecard. Because they have to be collected for external purposes and will

always receive much attention from shareholders, financial measures have in-bred

advantages with respect to top management attention and are bound to "creep up"

on top managers unless their attention is specifically focused in other directions as

well.

Implementation issues

Introducing a Balanced Scorecard means introducing a change in the company. This

is

never easy, and it is especially difficult when the change involves performance

reporting and risks modifying the balance of power within the organization.

Companies trying to implement Balanced Scorecards can encounter difficulties along

the following lines:

13

1.

The first problem that many firms encounter is the realization that the top

management team cannot articulate a clear and shared view of the firm's strategy; in

some cases, the strategy is not clear, in other cases members of the top management

team hold different views on what the strategy of the firm is or ought to be. The first

step of the process is thus to get to a consensus on what the firm should try to

achieve.

2.

Developing and maintaining a Balanced Scorecard can create workload for

many people. In particular, some of the data required may not currently exist within

the firm and thus needs to be collected specifically for the scorecard. Managers that

are often already stretched by their normal workload may not be enthusiastic about

this additional demand on their time. Furthermore, many companies have a track

record of starting and later abandoning initiatives like the Balanced Scorecard. As a

result some employees may have grown weary of such change efforts and may have

developed an attitude along the lines of "if I wait long enough, this will go away!".

Top managers interested in the Scorecard concept may thus encounter some

cynicism among their troops when they bring up the idea.

3.

Aside from resistance to increased workload for an initiative that may or may

not have clear benefits for the managers involved, companies may encounter

resistance motivated by a desire to protect one's turf or power base. Senior

managers should not assume that the absence of specific quantitative indicators in a

firm is always due to ignorance or excessive workload. In many cases, such absence

of information reflects what we call

opaqueness by design.

Local managers have

learned to develop secondary sources of information that are not accessible to top

management and/or to their subordinates. Maintaining opaqueness is often a way

for managers to centralize authority and/or to protect themselves from scrutiny and

questioning by their boss. The Balanced Scorecard highlights trade-offs and thus

brings increased transparency, which may be threatening for some managers.

4.

Once the Balanced Scorecard is developed, it must then survive and prosper

among competing reporting mechanisms. For this to happen, top management must

14

be consistent in its decision to widen their perspective from a narrow emphasis on

financial measures. In one company we studied, for example, a manager said: "we

developed a Balanced Scorecard and used it in our monthly discussions. This lasted

until the first time we failed to meet our financial targets, at which point we didn't

talk about the Balanced Scorecard anymore; we reverted back to talking only about

financial performance."

While the need for consistency is common-sense and easy to accept in

principle, displaying such consistency is not easy for top managers who have

reached their position in part because of their ability to reach financial targets. This

need for consistency is not specific to scorecards or Tableaux de Bord; the same

problem exists with any project that goes beyond short term financial results, e.g.,

Quality or Just-in-Time programs. Just as managers should not talk about quality for

all but the last two days of the month, they cannot expect subordinates to develop a

broader view of performance encompassing a more balanced scorecard if they do not

consistently reinforce this broader view themselves.

One way for top management to show focus and consistency in outlook is to

link employees' performance evaluation and reward to performance on the Balanced

Scorecard. Some companies have started doing so; the insurance company Cigna

Property and Casualty, for example, calculates its employees incentive compensation

based on a set of Balanced Scorecards.

8

Surveys by consulting firms also suggest that

an increasing number of large firms are tying executive compensation of senior

executives to balanced scorecard-types of indicators.

9

Other companies prefer to

gain more experience with their scorecard before creating a tight link with reward

systems. This "wait while we learn" approach is quite reasonable given the

enhanced resistance that changes to compensation systems tend to create, but it is

clear that companies that tie significant rewards with financial performance only are

using a dangerous "double talk" when they also try to emphasize a broader outlook

during balanced scorecard progress meetings.

8

See "Cigna P&C: A Balanced Scorecard",

CFO Magazine,

October 1996. For another example, see also

Robert S. Kaplan's case "Mobil USM&R (A): Linking the Balanced Scorecard" (HBS # 9-197-025).

9

See, for example, a 1996 study by Towers Perrin, New York, quoted in

HR Focus

(June 1996).

15

Role of the controller

The controller can support the scorecard development process in two very significant

ways because of the skills they have with respect to measurement and structured

reasoning.

Structured reasoning

On a recent consulting assignment we were asked to help the executive teams of

several business units to develop a more focused and performance oriented

approach to their business. (The project was similar to the (re)-introduction of a

management-by-objectives system). Our first contribution was to help these

managers be more rigorous in articulating their mission and their strategy, then in

translating them into a manageable subset of objectives; Executives often came up

with lists of 15 to 20 goals, which could in fact fit into 4 or 5 major blocks of related

initiatives.

Selecting the right performance indicators

The next step was for the managers to translate the objectives into measurable

targets, which many experienced as a very challenging process. Aside from sales

and manufacturing functions, many managers remain moderately skilled at

identifying quantifiable performance indicators. This process is not as easy as it

seems; the indicators must be controllable (i.e., target achievement should not be

overly influenced by events or decisions that are out of managers' control), but they

should also be reasonably complete (i.e., they should not fail to capture important

dimensions of performance such as cooperation with other business units or

adaptation to significant external events). Because of their experience and training,

controllers tend to be better skilled than line managers at identifying the right

performance indicators.

Conclusion

Balanced Scorecard and Tableaux de Bord are powerful tools. They have many

potential benefits which we have tried to describe in this article. Like all

16

management tools, however, the Balanced Scorecard is not a sufficient condition for

success; it cannot do everything! For example, it should not be a tool supporting

attempts at management-by-exception and management-from-a-distance. Neither is

it a substitute for sound strategy, clear focus and strong alignment of energies within

the firm. On the other hand, developing and using a Balanced Scorecard-type of

system can help develop these conditions by forcing top management to articulate a

strategy and Key Success Factors, and focusing managers' attention on the firm's

progress on these elements. To achieve these benefits, top management needs to

show focus and consistency: Focus during the design of the tool, and consistency

when using it.

17

FINANCIAL

"To succeed

financially,

how should

we appear

to our

shareholders?"

CUSTOMER

INTERNAL BUSINESS PROCESS

"To achieve our IObjectives Measures

I

Targets

I

Initiatives

vision, how

should we

appear to our

customers?"

Objectives i Measures

I

Targets

i Initiatives

I

I

I

I

7

"To satisfy our

shareholders

and customers,

what business

processes must

we excel at?"

I

I

I

I

I

I

I

I

I

I

LEARNING AND GROWTH

Objectives

I

Measures

I

Targets

I

Initiatives

1

"To achieve our

vision, how

will we sustain

our ability to

change and

improve?"

Objectives

I

Measures

I

Targets

I

Initiatives

I

I

I

I

I

I

I

I

Vision and

Strategy

Figure 1

Translating Vision and Strategy: Four Perspectives*

* Reprinted from

"Linking the Balanced Scorecard to Strategy",

by Robert S. Kaplan and David P. Norton, California Managment Review (July 1996)

Employee

Suggestions

Shorter

Cycle

Lower

Time-'4"'N‘

'b■- Rework

Process Quality

Financial

Customers

Internal

Business

Processes

Learning and

Growth

Figure 2

Organizing Performance Indicators in a Causal Chain

* Adapted from "Using the Balanced Scorecard as a Strategic Management System" by Robert S. Kaplan and David P.

Norton, Harvard Business Review (January-February 1996)