Your Guide to Homeowners Insurance – For Michigan Consumers Page 1

Your Guide to Homeowners Insurance – For Michigan Consumers Page 2

Your Guide to Homeowners Insurance – For Michigan Consumers Page 3

Table of Contents

Page 4

Understanding Your Homeowners Insurance Policy

Page 5

Sample of a Declarations Page

Page 6

Insurance Eligibility

Page 7

Types of Policies

Page 8

Settlement Options Found in Homeowners Policies

Page 9

Types of Coverage

Page 10

Extra Coverages You Can Purchase

Page 12

Understanding Rates and Premiums

Page 13

Ways to Reduce Your Premium

Page 14

If You Experience a Loss

Page 15

Page 16

Shopping for Coverage

Filing a Complaint with DIFS

Page 17

Insurance Worksheets

Page 20

Homeowners Insurance Company Web Addresses

Page 21

Glossary of Common Homeowner Insurance Terms

This Consumers Guide is a publication prepared by the Michigan Department of Insurance and

Financial Services (DIFS). You can view more publications by visiting DIFS’ website at

www.michigan.gov/difs

.

Any insurance consumer who needs help with an insurance problem or question can call DIFS

for assistance toll-free at 877-999-6442.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 4

Understanding Your Homeowner’s Insurance Policy

Your insurance policy is a contract between you and your insurance company. It specifies what the

company agrees to do in exchange for the premium you pay. It also describes your responsibilities and

the terms of coverage. The contract is divided into two basic sections: a declarations page and the

policy itself.

The Declarations Page

The declarations page is usually the first part of an insurance policy and includes basic details of the

agreement such as:

• Name of the insurance compan

y

• Nam

e(s) of the person(s) insured

• Location of the insured residenc

e

• T

he policy number

• Property covered

• Coverages purchased

• Limits of liability for each coverage

• Applicable deductibles and

• Your premium

The Policy

The second part of your insurance contract is the policy itself. This includes:

• Insuring agreements

• Definitions

• Conditions

*Section I of your policy describes your property coverages and the perils it covers. Section II

typically includes:

• Liability coverage (protection

against claims someone else

makes against you)

• Premises medical coverage or

accidental injury coverage (pays

the medical expenses of others

accidentally injured on your

property)

Each section includes coverages,

limitations, exclusions, definitions, and

conditions that apply only to that

section.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 5

Sample Declarations Page

Your Guide to Homeowners Insurance – For Michigan Consumers Page 6

Insurance Eligibility

Michigan law defines an “eligible person” for homeowners

insurance as a person who is the owner living in, or a tenant of,

one of the following types of dwellings: a house, condominium

unit, cooperative unit, room, apartment, or a multiple unit

dwelling of not more than four residential units.

However, you may still be considered “ineligible” and can be

turned down for insurance if:

Within the past 5 years you have been found guilty of

arson or of an attempt to commit arson, the use of

explosives, or destroying property.

Within the past 5 years you have been denied payment

by an insurer of a claim under a home insurance policy

based on evidence of arson, fraud, or conspiracy to

commit arson or fraud.

The property you want to insure is used for illegal or dangerous purposes.

Taxes on the property you want to insure are 2 or more years past due.

You refuse to buy the minimum amount of coverage required for the type of policy you want.

Your home has a physical condition which presents an extreme likelihood of a significant loss

under a home insurance policy.

Within the past 2 years your home insurance has been canceled because of non-payment of

premium, unless you pay the entire premium in full before the issuance or renewal of the policy.

A company requires you to be a member of a group, club, or organization and you choose not

to join or maintain membership.

If the value of the property you want to insure does not meet the minimum requirements for the

type of policy you want to buy.

If you find that you are ineligible for home or renters insurance, you may want to ask your agent to apply

to the Michigan Basic Property Insurance Association (MBPIA). The MBPIA was created by the state

legislature to provide property insurance to persons who cannot find insurance in the regular market.

Any licensed agent can help you obtain insurance through the MBPIA.

Do I Have to Carry Insurance on a Home?

Unlike some other insurance coverages, you are not required by law to purchase homeowners

insurance. However, if you are financing your home, your lender will require you to purchase insurance

to protect its financial interest. Lenders will buy an insurance policy to cover your home if you don’t

maintain insurance coverage in accordance with the terms of your loan agreement. The loan

documents you sign may require you to maintain coverage. If coverage is required but not maintained,

the lender will place coverage on the property called force-placed insurance, to protect their interest

in the property and charge you for this coverage.

The loan documents will spell out specifically what must be covered and how proof of coverage is to be

submitted to the lender or the company servicing the loan. If your home is not being financed, you may

If you are eligible under

the law you cannot be

denied insurance solely

because of the age of

your house, its location,

or the type of

neighborhood you live

in.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 7

choose not to purchase homeowners insurance, but you will be assuming all the risk to replace your

home and possessions if they are damaged.

Types of Policies

The main types of homeowners insurance are:

Broad (HO-2) covers damage to the

dwelling and possessions from specific

perils listed in the policy such as

explosion, fire, lightning, windstorm, hail,

riot, civil commotions, theft, vandalism,

falling objects, smoke, and damage

from a vehicle or aircraft. “Broad” form

policies are also known as “named

peril” policies.

All Risk (HO-3) is the most common type

of homeowners policy. The dwelling is

covered against all risks or perils except

those specifically excluded in the

policy. The home’s contents are

generally covered against named

perils.

Renters (HO-4) policies provide coverage on the renter’s personal property if it is stolen, damaged, or

destroyed in a home or apartment. Personal property is covered against named perils, and losses are

settled on an actual cash value basis unless the renter purchases replacement cost coverage. Renter

policies do not cover the house or apartment building or any detached structures.

Condominium (HO-6) policies provide coverage similar to a renter’s policy since the limit chosen is based

on the value of the owner’s personal property or contents.

An HO-6 policy also provides coverage for that part of the dwelling that belongs to the condominium

owner; this includes alterations, appliances, fixtures and improvements that are part of the building or

are contained within the building. Both the dwelling and the contents are covered against named perils.

Additional coverage may be added to a policy through attachments known as endorsements, floaters,

or riders to extend protection to specific items you own. Ask your insurance agent about buying

endorsements for an additional premium if you would like more coverage than your policy provides. The

availability of endorsements varies by company.

Other Types of Policies

Mobile homeowners policy

Policies are similar to those of conventional homes but have additional provisions specific to mobile

homes. They usually include the cost of moving your home to avoid damage from floods, windstorms,

and other perils.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 8

Farm or ranch policy

Policies are similar to those of homeowners but include special additions for farm or ranch buildings

and equipment.

Travel trailers, camping trailers, and motor home policy

They are insured under automobile, recreational vehicle, or special policies.

Settlement Options Found in Homeowners Policies

It is important to know the difference between

replacement cost, repair cost, and actual

cash value when it comes to insuring both your

home and your possessions. Most

homeowners insurance policies will give you

the choice to cover contents on a

replacement cost basis or an actual cash

value basis. However, there are also policies

available that provide for settlement on a

repair cost basis.

Replacement cost is the cost to replace, repair

or rebuild your home to its original condition

with materials of the same kind and quality if it

is damaged or destroyed. For example, a hardwood floor would be repaired or replaced with hardwood

rather than a laminate or other material. Replacement cost coverage pays the full cost of replacing

your property, minus your deductible, and up to your policy’s dollar limit. A standard homeowners policy

contains a limit on the replacement value. If your limit is less than what it would take to rebuild your home

at current construction material and labor costs, you may want to increase your policy limit.

Repair cost is the cost to replace, repair or rebuild damaged dwellings to a similar condition, using

contemporary materials. For example, plaster walls may be replaced with drywall. The maximum amount

the insured is able to collect may not be enough to repair or replace the property to its original condition.

Make sure you discuss the coverage in detail with your insurance agent to ensure that you understand

the loss settlement provisions thoroughly.

Actual cash value is the replacement cost of the property at the time of loss minus depreciation. This

means the insurance company will subtract an amount for depreciation from the value of your

possessions before paying your claim. For example, actual cash value on a 10-year-old television may

only be $50. Replacement cost is what it would cost to replace it with a similar model today, which would

be substantially more than $50. Replacement cost minus depreciation equals actual cash value.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 9

Types of Coverage

There are seven major coverage parts of a typical policy: Coverage A, B, C, D, E, F and G. The coverage

parts are complex with many exclusions and limitations. Price is only one factor to consider when

selecting your insurance. Consider purchasing homeowners insurance at a sufficient level so that, if there

is a need to file a claim, there are no surprises or gaps in your coverage.

Dwelling (Coverage A)

This coverage protects against loss to the dwelling. Except for repair cost policies, a loss which occurs to

an insured dwelling is typically settled on a replacement cost basis.

Appurtenant Structures (Coverage B)

Other structures on the property, such as a detached garage, tool shed, barn, or swimming pool are

usually covered for up to 10% of the dwelling amount with no extra premium charge.

P

ersonal Property/Contents (Coverage C)

This coverage protects against loss to personal property in amounts which vary, depending on the policy

form type. Covered loss of personal property is usually settled on an actual cash value basis. However,

many companies offer replacement cost coverage on personal property for additional premium.

Off-Premises Loss

There is also protection against loss to personal property while away from the premises, such as

property left in a car or hotel room. Usually the coverage is limited to 10% of the total contents

coverage amount.

Special Items

There are special limits on coverage for certain items such as money, jewelry, computers, or furs.

These limits vary by company and do not increase the total amount of coverage under the policy.

A

dditional Living Expenses (Coverage D)

The additional living expenses portion of your homeowners insurance policy pays for extra expenses

homeowners incur if they have to live away from their home following an insured risk. Expenses paid

include hotel or apartment bills, restaurant meals and even lost rent if you rent out part of your house.

Coverage for additional expenses is typically 20% of the insurance on your house.

Liability (Coverage E)

This coverage provides protection in the event you become legally obligated to pay for bodily injury or

property damage. For example, if you were sued by someone injured on your property, this coverage

will pay to defend you and provide coverage if you are determined to be liable.

M

edical Payments (Coverage F)

This coverage pays for immediate care, such as first aid, ambulance charge, etc., for someone who is

hurt on your property. The amount of coverage offered depends on the company.

Property of Others (Coverage G)

Replacement cost coverage is provided for physical damage to the property of others that is caused

by the insured. The amount of coverage is dependent on each insurer.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 10

Extra Coverages You Can Purchase

There are some additional coverages that may be available to purchase through your insurer to

enhance your coverage. It is important for you to speak with your agent if you are interested in

purchasing additional coverage for your property.

A

dditional Replacement Cost Coverage

Additional replacement cost coverage for the dwelling may be purchased under certain types of

homeowners policies. Under this additional coverage, the company guarantees that you will be

protected for the full replacement cost of the house, even if that amount is higher than the policy limit.

Some companies refer to this coverage as “extra expense” coverage or “guaranteed replacement

cost” coverage. Check with your agent to find out the specific limits of this additional coverage.

Debris Removal

If debris removal expense plus damage to the property is more than the limit of coverage selected, an

additional 5% of the coverage limit may be available for debris removal. This is coverage provided for

the reasonable expense incurred for removal of debris of covered property after a covered loss.

T

ree Removal

This coverage will pay to have damaged trees removed; the standard limit is $500. Many companies

require the tree to have actually fallen or caused damage to other property due to a covered peril

before coverage is provided.

T

rees, Shrubs, and Other Plants

This coverage will pay the cost to replace damaged trees, shrubs and other plants; the standard limit is

$500 per item up to an aggregate limit.

F

ire Department Service Charge

This coverage pays expenses when the fire department is called to save or protect covered property;

the standard limit is $500.

Credit Card, Fund Transfer Card Forgery, and Counterfeit Money

This coverage protects against the fraudulent use of credit cards or fund transfer cards (money machine)

or reimburses you if you accidentally receive counterfeit money; the standard limit is $500.

O

rdinance and Law Coverage

This provides extra coverage if your home is partially damaged and cannot be rebuilt to its original

condition because of changes in the local building codes. The insurance company will not pay for the

upgrades unless you have this additional coverage. The standard limit is 10% of the total dwelling

coverage amount, but some companies will allow you to purchase larger amounts.

P

ersonal Property Endorsements

These endorsements provide extra insurance, up to the value of the insured property, for items that

exceed the amount listed for such property in your regular policy. You may need to purchase this

additional coverage for items such as expensive jewelry, cameras, collections, laptop computers, or rare

antiques. Most insurers require you to have such items appraised to determine their value at the time

you purchase the insurance.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 11

Water Backup and Sump Pump Overflow

Read your policy carefully for coverage and exclusions relating to water damage. You may need to

purchase additional coverage for damage resulting from water backup and sump pump overflow.

Flood Insurance

Your regular homeowners insurance policy does not contain coverage for flood damage to

your home and contents. In order to have coverage in the event of a flood, you must purchase

an additional flood insurance policy. Your agent should be able to advise you about how to

purchase this coverage as well as the amount of coverage you need. You may also call the

National Flood Insurance Program for more information at 800-427-4661 or visit www.floodsmart.gov.

Private flood insurance may also be available.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 12

Understanding Rates and Premiums

Insurance companies use rating factors to determine the premium they will charge you for your policy.

Rating rules are used to give the company the ability to charge the correct rate for the risk they are

insuring and to apply discounts fairly among their policyholders.

I

n addition to rates, companies develop guidelines called underwriting rules to decide if a risk qualifies

for coverage. Each company’s guidelines may differ, but their underwriting rules and rates must be

applied uniformly and consistently throughout Michigan.

Factors That Affect Your Premium

An insurance company uses the process of underwriting to determine whether to sell you a policy and

what premium to charge. Different factors can positively or negatively affect your premium. Insurance

companies use many factors to determine the amount of premium you pay. These factors may include

such things as:

• A

mount and type of coverage. Your premiums will increase in relation to the amount of coverage

you choose to purchase to protect your home, property, and assets.

• Your home’s age and condition. The premium is often higher for an older home or one in poor

condition than it is for a newer home in good condition.

• Your claim history. Your claim history includes both the type and the number of claims filed. Your

history of filing claims for water damage, fire, theft, or liability on homes you have owned is used

by the insurance company to determine what to charge for your coverage.

• Construction material used in your home. The insurance premium is usually lower for homes built

primarily of brick or masonry than for wood-frame homes.

• Availability of local fire protection. Homes in areas with access to quality community fire

protection and a nearby water source usually have lower premiums.

• Availability of law enforcement or crime prevention services. Premiums may be lower if your home

is in proximity of regular and available law enforcement patrol.

• Where you live. The law allows insurance companies to divide the state into rating territories.

Premiums could be higher for homes in areas with higher crime rates, high storm activity, or higher

claims history.

• The cost to rebuild your home. If your home is destroyed, your policy will pay to rebuild your home

,

depending on the policy limit, at current construction material and labor costs. This is not the same

as the purchase price of your home which includes the cost of the land. Your premiums will

increase in relation to the amount of your replacement cost coverage.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 13

Ways to Reduce Your Premium

Discounts

Companies may offer premium discounts based on factors that are likely to reduce losses or expenses.

Each insurance company sets the amount of discounts it offers. Common discounts offered by many

companies include:

• Paid in full discount

• Mature homeowner discount (age of maturity varies by insurance company)

• Claim free discount

• Non-smoker discount

• New home discount

• Credit-based insurance score discount

• Multi-policy discount

• Protective Devices (smoke detectors, fire extinguishers, burglar alarms, heavy duty locks, etc.)

Increased Deductibles

You may want to consider the largest deductible your budget can handle to lower your premium.

How Discounts Affect Your Premium

The example below represents a standard base premium a person may have to pay for an HO-3 policy

(All Risk) if they do not qualify for any discounts. The discount is applied separately, totaled and then

deducted from the base premium. Our example shows how dramatically the premium has changed.

However, you may not qualify for each of the discounts offered in this example or your insurance

company may not offer all of these discounts. The example illustrates how important it is for each

homeowner to shop for coverage with several different companies and inquire about all discounts for

which they may be eligible.

Base Premium

$1,510

Smoke Detector Discount

2%

-30

Deadbolt Lock Discount

2%

-30

Fire Extinguisher Discount

2%

-30

New Home Discount

20%

-302

Auto/Home Multi-policy Discount

17%

-257

Life/Home Multi-policy Discount

5%

-76

Credit-Based Insurance Score 7

6%

-91

Mature Homeowner Discount

3%

-45

Final Premium

$649

T

his company offers several levels of discounts for a new home. For example, a 2-year-old home still has

a new home discount, but it will decline annually until the home reaches 10 years of age at which time

the discount ends. In the example, the applicant received a credit-based insurance score of 7 and a

discount of 6% off the base premium. For this company, a score of 7 is a medium range discount.

However, each company uses a different scoring methodology so be sure to ask your agent about your

insurance score and how it affects the premium you are being quoted.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 14

Home Insurance Discounts by Company

Companies add new discounts frequently. Be sure to ask for a list of discounts that are offered from

each company you are considering for the purchase of homeowners insurance. Most companies

have a cap on the total amount of discounts that a person can use to reduce their premiums.

For example, if you qualify for several discounts that amount to over 90% of the premium, the

company may limit the total amount of discounts you can claim to 50% of the premium.

Prepare Ahead to Ease the Claims Process

Insurance is something you hope you never have to use; but, if you should ever need to file a claim

after experiencing a loss of property from fire, theft, or other cause, take steps now to make the

process of filing a claim easier.

• W

ritten inventory - Create and regularly update a written inventory of your home’s contents. Your

insurance company may have a home inventory checklist available to help you compile an

accurate inventory of your possessions or use the National Association of Insurance

Commissioners’ (NAIC) downloadable home inventory checklist.

• Receipts - Keep copies of receipts to document items purchased, date and cost.

• Video/photographic record - Videotape or photograph the contents of your home and the

exterior from different viewpoints and angles. Include video/photos of each room, closet,

cabinet, drawer, garage, attic, and separate buildings from the residence.

• Document security – Keep your insurance policy, home inventory, appraisals, photos and video

records in a secure secondary location (such as your office or a safety deposit box). Update your

records and documentation annually.

• Appraisals – Have someone appraise your jewelry, antiques, stamps, coins, and other valuable

collectibles.

If You Experience a Loss

• Notify your agent or insurance company immediately and report losses involving theft or crime to

the police.

• Review your policy and ask your agent or insurance company if you have any questions regarding

coverage dollar limits.

• Ask your agent or insurance company what documents, forms, and other data you need to get

your claim processed. Complete and submit all forms in a timely and accurate manner to prevent

claim processing delays.

• Make a detailed list of your damaged property by itemizing your losses. If possible, photograph or

videotape the damage before making any repairs.

• Make only temporary repairs to protect your house and belongings from further damage. Save

the receipts for temporary repairs and submit them to the insurance company for reimbursement.

You should not make permanent repairs until after your insurance company has inspected the

damaged property.

• Tell your agent or insurance company where they can reach you.

• Write down the date, name, and title of the person you spoke with and what was said whenever

you communicate with your insurance company in-person or on the telephone.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 15

Shopping for Coverage

Take the time to shop around for your homeowners

insurance. You may be surprised at how much money you

can save if you pick up the phone or go online to obtain

quotes from several companies. Remember, insurance

quotes are not binding and the actual price is determined

after the insurance company receives your application and

completes the underwriting process, which may include an

inspection of your dwelling.

To get an accurate quote, you will need the following types of information:

Construction materials

Type of floor plan

Number and types of rooms

Type of garage or carport

Total square footage

Fire and security devices

Distance from the nearest fire department and hydrant

Loss history

Questions to ask:

How much would I save if I increase my deductible?

Does coverage include water damage or sewer backup?

What is the difference between flood insurance and water damage or sewer backup

insurance?

Is my coverage replacement cost or repair cost?

Are my dependents living away from home covered under my policy?

Does the policy cover my jewelry, antiques, or special collections?

What other special coverages are available?

What proof do I need in case of loss?

What discounts might I be eligible for?

Your Guide to Homeowners Insurance – For Michigan Consumers Page 16

Filing

a Complaint with DIFS

DIFS provides consumer information and investigates consumer complaints against insurance, banking,

credit union, mortgage and other consumer financial products. DIFS will work to respond promptly and

completely to consumers’ insurance and financial questions and complaints, assist consumers in

resolving those complaints whenever possible, and help consumers understand their options.

DIFS first encourages consumers to attempt to resolve disputes directly with their insurance and/or

financial service entity. If a resolution cannot be reached, DIFS can help try to resolve your dispute.

• Speak with a company representative to try to find a solution.

• Explain the problem in a calm, courteous manner.

• Provide dates, amounts, and as many related facts as you can

.

I

f you still do not agree with the company’s position, ask them to provide a written response. Ask them

to list the specific rules or language in the policy that allow them to deny or exclude coverage.

If you feel that your insurance agent misrepresented what your policy covers, made false statements

to persuade your decision about coverage, or used other dishonest methods, try to resolve the dispute

by speaking directly with the agent.

If you still do not agree with the agent’s position, ask for a written response. Ask the agent to include

policy language, copies of documents you signed when you applied for insurance, or other reasons or

facts, which might support the agent’s actions.

How DIFS Can Help

If you are still dissatisfied after contacting the company or the agent, you may wish to contact DIFS,

Office of Consumer Services, to ask questions or to file a written complaint. For more information please

contact DIFS at 877-999-6442 or visit www.michigan.gov/DIFS

.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 17

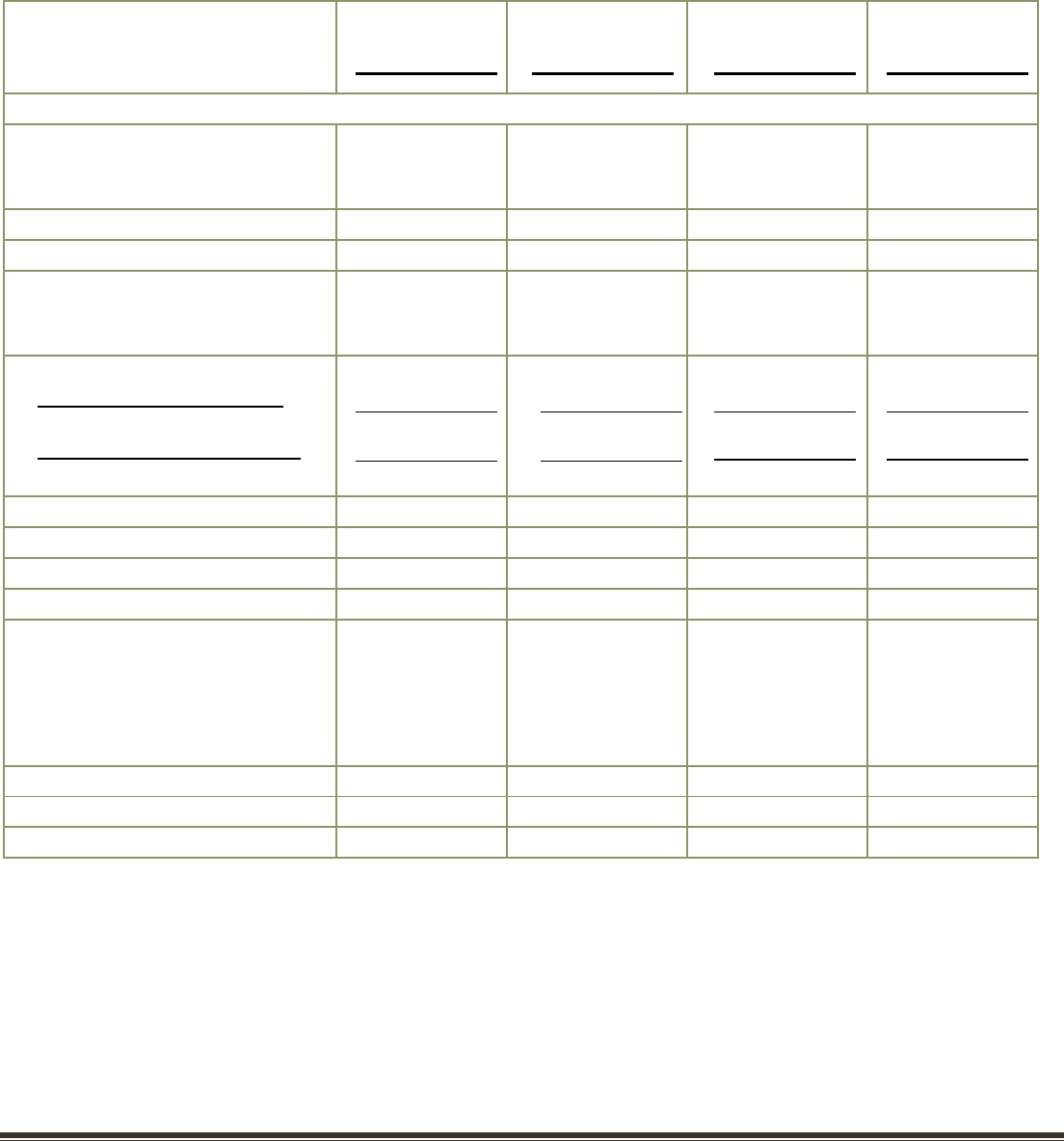

Insurance Worksheet for Homeowners

Use this chart to compare the quotes you receive from insurers and to explore the available options. In

order to accurately compare policies, you will need to indicate what each company includes for each

of the coverages in their policy limits. For example, Company A may have a $500 standard deductible,

while Company B may have a $1000 deductible for the same total premium. To make accurate

comparisons you will need to make sure all values are equal or decide which items you are willing to

pay more for if you increase the limit.

Coverage (HO-2 or HO-3)

Company A

Company B

Company C

Company D

Home Repair Cost (HO-2) or

Replacement Cost (HO-3)

dwelling limit

Personal Liability

Deductible

Appurtenant Structures

(unattached garage,

outbuildings, etc.)

Contents:

Replacement Cost (RC)

or

Actual Cash Value (ACV)

Off-premises Contents

Additional Living Expenses

Medical Payments

Property of Others

Discounts Offered by

Company – List each discount

for which you qualify and the

amount it will reduce your

premium.

Annual Premium

*An HO-3 may have either replacement cost or actual cash value settlement options for contents. In order

to make a complete comparison among policies, be sure to identify which settlement option the company

uses for contents. Replacement cost content policies may be more expensive.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 18

Insurance Worksheet for Homeowners (continued)

The chart below lists optional coverages that you can usually purchase for a fee with your home

insurance policy. You will have to determine what coverage is most appropriate for your particular

lifestyle.

Coverage

Company A

Company B

Company C

Company D

Guaranteed Replacement

Cost

$

$

$

$

Ordinance and Law Coverage

$

$

$

$

Debris Removal

$

$

$

$

Credit Card, Fund Transfer,

Counterfeit Money

$

$

$

$

Sewer and Drain Backup

$

$

$

$

Scheduled Personal Property

$

$

$

$

Tree Removal

$

$

$

$

Trees, Shrubs and Other Plants

$

$

$

$

Fire Department Service

Charge

$

$

$

$

Other

Additional Premium:

$

$

$

$

Your Guide to Homeowners Insurance – For Michigan Consumers Page 19

Insurance Worksheet for Renters (HO-4) and Condominium Owners (HO-6)

Coverage (HO-4 or HO-6)

Company A

Company B

Company C

Company D

Dwelling Coverage (HO-6 only)

Contents:

Replacement Cost (RC) or

Actual Cash Value (ACV)

Personal Liability Amount

Standard Deductible Amount

Off-Premises Contents

Additional Living Expenses

Medical Payments

Property of Others

Loss Assessment (HO-6 only)

Discounts Offered by

Company-- List each discount

for which you qualify and the

amount it will reduce your

premium.

These are additional coverage options you can purchase with your HO-4 or HO-6 insurance policy.

Each option will add cost to the standard policy premium. You will have to determine what coverage

is most appropriate for your particular lifestyle.

Credit Card, Fund Transfer,

Counterfeit Money

Scheduled Personal Property

Others

Annual Premium:

Your Guide to Homeowners Insurance – For Michigan Consumers Page 20

Home Insurance Company Web Addresses

Most insurers offer websites which allow consumers to shop for home insurance and obtain insurance

quotes. DIFS asked insurance companies participating in the discount survey to provide us with their

website address and phone number. The following list of company website addresses or phone numbers

are being provided as an additional shopping tool.

Allstate Indemnity Company

www.allstate.com / 866-621-6900

Allstate Insurance Company

www.allstate.com / 866-621-6900

Allstate Property and Casualty Ins. Co.

www.allstate.com / 866-621-6900

Allstate Vehicle and Proper Ins. Co.

www.allstate.com / 866-621-6900

American Bankers Ins. Co. of Florida

877-584-1364

American Family Home Ins. Co.

www.AMIG.com

American Modern Select

www.AMIG.com

American Security Ins. Co.

877-893-5739

Armed Forces Insurance Exchange

www.afi.org

Auto Club Group Ins. Co.

www.michigan.aaa.com/insurance

Auto-Owners

www.auto-owners.com

Automobile Ins. Co. of Hartford, CT.

www.travelers.com

Bankers Standard Ins. Co.

800-444-6161

Central Mutual Insurance Co.

www.central-insurance.com

Cincinnati Ins. Co.

www.cinfin.com

Citizens Insurance Co. of American

www.hanover.com

Depositors Insurance Co.

800-982-0756

Electric Insurance Co.

800-227-2757

Encompass Indemnity Co.

www.encompassinsurance.com

Encompass Property and Casualty Co.

www.encompassinsurance.com

Farm Bureau General Insurance Co. of MI

www.farmbureauinsurance-mi.com

Farmers Insurance Exchange

www.farmers.com

Fidelity and Deposit Co. of MD

800-660-4539

Fire Insurance Exchange

www.farmers.com

Hastings Mutual Insurance Co.

www.hastingsmutual.com

Homesite Insurance Co.

www.homesite.com / 800-466-3748

Homesite Insurance Co. of the Midwest

www.homesite.com / 800-466-3748

IDS Property Casualty Insurance Co.

www.ameriprise.com/autohome

Kemper Direct (formerly Unitrin Direct)

www.kemperdirect.com

MemberSelect Insurance Co.

www.michigan.aaa.com/insurance

Metropolitan Property and Casualty Ins. Co.

866-482-5546

Michigan Insurance Co.

www.michiganinsurancecompany.com

Mutual Aid Exchange

www.maxinsurance.com

Pharmacists Mutual Insurance Co.

www.phmic.com / 800-247-5930

Praetorian Insurance Co.

800-660-4539

Privilege Underwriters Reciprocal Exchange

www.pureinsurance.com

QBE Insurance Corporation

800-660-4539

State Automobile Mutual Ins. Co.

www.stateauto.com

State Farm Fire and Casualty Co.

www.statefarm.com

Teachers Insurance Co.

www.horacemann.com

Travelers Indemnity Co. of America

www.travelers.com

Trumbull Insurance Co.

800-824-8822

Wolverine Mutual Insurance Co.

www.wolverinemutual.com

Your Guide to Homeowners Insurance – For Michigan Consumers Page 21

Glossary of Common Homeowner Insurance Terms

A

Actual Cash Value (ACV) — The value of your property, based on the current cost to replace it minus

depreciation. Also see “replacement cost.”

Additional Living Expenses (ALE) — The additional living expenses portion of your homeowners insurance

policy pays for extra expenses homeowners incur if they have to live away from home following an

insured risk. Expenses paid may include hotel or apartment bills, restaurant meals, or lost rent if you rent

out part of your house. Coverage for additional expenses is typically 20% of the insurance on your house.

A

djuster — An individual employed by an insurer to evaluate losses and settle policyholder claims. Also

see “public insurance adjuster.”

Agent — A person who sells insurance policies.

All Risk — Coverage against “all risks” means that losses are covered for any reason except for those

specifically excluded in the policy. Those risks excluded could be items such as flood, war, collapse, and

water and sewer backup.

Application — A form you fill out with information about you that an insurance company will use to

decide whether to issue you a policy and how much to charge.

Appraisal — An evaluation of home insurance property by an authorized person to determine property

value or damaged property value.

B

Binder — A temporary insurance contract that provides proof of coverage until you receive a

permanent policy.

Broad Form Insurance — Coverage is provided for the named perils specified in your policy. “Broad”

form policies are also known as “named peril” policies.

C

Cancellation — Termination of an insurance policy by the company or named insured before the

renewal date.

Claim — A policyholder’s request for reimbursement from an insurance company under a home

insurance policy for a loss to property.

Claimant — A person who makes an insurance claim.

Contract — An insurance policy. A policy is considered to be a contract between the insurance

company and the policyholder.

Coverage Amount — The dollar amount that is covered by the insurance company.

Credit-Based Insurance Score — This score is a rating based in whole or in part on a consumer’s credit

information. An insurance score is not the same as a credit score. Using a mathematical formula, a

consumer’s credit characteristics are put through a scoring model that assigns weights to various factors

to determine an “insurance score.” The resulting score is indicative of the likelihood the consumer will file

a claim, not his/her ability to pay the premium. The scoring models are developed by modeling firms

such as Fair Isaac and ChoicePointe or by individual insurers.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 22

D

Declarations Page — Usually the first page of an insurance policy, it contains the full legal name and

address of the insurer, name and address of the insured, the policy number, the period of time a policy

is in force, the amount of the premium, and the amount of coverage.

Deductible — The amount the insured is responsible to pay for a loss before any payment is due from the

insurance company.

Depreciation — Decrease in the value of property over time due to use or wear and tear.

E

Effective Date — The date on which coverage under and insurance policy begins.

Endorsement — A written agreement attached to a policy expanding or limiting the benefits otherwise

payable under the policy. The purpose of the endorsement, also called a “rider,” is to modify the original

agreement to fit the needs of one specific policyholder.

Exclusion — A provision in an insurance policy that denies coverage for certain perils, people, property,

or locations.

Expiration Date — The date on which coverage provided by an insurance policy ends.

F

Force-Placed Insurance — Insurance coverage for only one of the parties having an insurable interest in

that property. For instance, if you still owe money on your mortgage and do not have homeowners

insurance, your lender may take out a single interest insurance policy to protect its own interest in your

property. This type of insurance protects only the lender, not the homeowner and is also known as lender-

placed insurance.

H

Homeowner Policies — Property insurance policies that provide a package of coverage such as

property damage protection, liability insurance, coverage for additional living expenses, etc.

I

Independent Adjuster — A person who charges a fee to an insurance company to adjust a claim on

behalf of the insurer.

Inflation Protection — Automatically adjusts your home insurance policy limits to account for increases in

the costs to repair or rebuild a property.

Insured — The person(s) entitled to covered benefits in the event of a loss.

Insurer — The insurance company.

L

Lapse — The termination of an insurance policy because a renewal premium is not paid.

Liability Coverage — Covers losses for which an insured is legally liable. For homeowners insurance,

liability coverage protects you against financial loss if you are sued and found legally responsible for

someone else’s injury or property damage.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 23

Loss — The dollar amount associated with a claim.

Loss of Use — A provision in homeowners and renters insurance policies that will reimburse policyholders

for the additional costs (housing, food, and other essentials) of having to live elsewhere while the

property is being restored following a loss.

Loss History — Refers to the number of insurance claims previously filed by a policyholder. A company

will consider loss history when underwriting a new policy or considering a renewal of an existing policy.

Companies view loss history as an indication of the likelihood that an insured will file a claim in the future.

M

Market Value — The current value of your home, including the price of land.

Material Misrepresentation — A significant misstatement in an application form. If a company had

access to the correct information at the time of application, the company might not have agreed to

accept the application or would have issued the policy at a different premium.

N

Named Perils — A type of insurance policy that names specific risks or “perils” covered by the policy.

These include fire, theft, smoke, lightning, riot, explosion, wind, falling objects, vandalism, etc.

Non-renewal — A decision by an insurance company not to continue a policy after its expiration date.

O

Optional Coverages – Endorsements to a policy that provide additional protection against losses that

would not otherwise be covered under the policy. The policyholder must pay an additional premium for

this coverage.

P

Peril — A specific risk or cause of loss covered by an insurance policy, such as a fire, windstorm, flood, or

theft.

Personal Property — All tangible possessions (other than land) that are either temporary or movable in

some way, such as furniture, jewelry, electronics, etc.

Policy — The contract issued by the insurance company to the insured.

Policyholder — The person or party who owns an individual insurance policy. This person may be the

insured, the beneficiary, or another person. The policyholder usually is the one who pays the premium

and is the only person who may make changes to a policy.

Policy Period — The time a policy is in force, from the beginning or effective date to the expiration date.

Premium — The amount paid by an insured to an insurance company to obtain or maintain an insurance

policy.

Property Damage — Physical damage to your dwelling and personal belongings.

Property Insurance — Coverage that protects your dwelling and personal belongings in case of fire,

theft, vandalism, etc.

Public Insurance Adjuster — An individual hired by a policyholder to negotiate a claim with the insurance

company in exchange for a percentage of the claim settlement. Public insurance adjusters must be

Your Guide to Homeowners Insurance – For Michigan Consumers Page 24

licensed by DIFS, use an approved DIFS form, and can only charge a maximum of 10% of the claim

proceeds.

R

Rating Territory — The local area within the state where the dwelling is located. It is usually defined by zip

codes.

Refund — An amount of money returned to the policyholder for overpayment of premium or if the

policyholder is due unearned premium.

Reinstatement — The process by which an insurance company puts a policy back in force.

Renewal — Continuation of a policy after its expiration date.

Renters Insurance – Coverage for a person’s personal property against specific perils in a home or

apartment owned by someone else. It also provides personal liability coverage and additional living

expenses. Possessions can be covered for their replacement cost or the actual cash value, which

includes depreciation. Renters policies do not cover the house or apartment building or any detached

structures.

Repair Cost — The cost necessary to replace, repair, or rebuild damaged property to a condition similar

to what it was before the damage, using contemporary materials. For example, plaster walls may be

replaced with drywall.

Replacement Cost — The cost necessary to replace, repair, or rebuild the structure or damaged property

to its original condition with materials of the same kind and quality without deducting for depreciation

but limited by the policy’s maximum dollar amount. For example, a hardwood floor would be repaired

or replaced with the same kind of wood.

Residual Market — Insurers, such as assigned risk plans and the Michigan Basic Property Insurance

Association (MBPIA), which exist to provide coverage for those who cannot get it in the standard market.

Rider — A written agreement attached to the policy expanding or limiting the benefits otherwise

payable under the policy; also called an “endorsement”.

S

Surcharge — An extra fee added to your premium by an insurance company.

U

Underwriter — The person who reviews an application for insurance and decides if the applicant is

acceptable and at what premium rate.

Underwriting — The process an insurance company uses to decide whether to accept or reject an

application for a policy and what rate to charge.

Your Guide to Homeowners Insurance – For Michigan Consumers Page 28

Department of Insurance and Financial Services 08/2019

P.O

. Box 30220

Lansing, MI 48909-7720

Toll-Free 877-999-6442