Financial

Report

OF the United States

Government

This page is intentionally blank.

Contents

A Message from the Secretary of the Treasury

Results in Brief ...................................................................................................

i

Executive Summary ...........................................................................................

1

Management’s Discussion and Analysis ..........................................................

8

Statement of the Comptroller General of the United States ..........................

36

Financial Statements

Introduction .......................................................................................................

46

Statement of Net Cost ........................................................................................

53

Statement of Operations and Changes in Net Position ......................................

55

Reconciliations of Net Operating Cost and Budget Deficit ...............................

57

Statements of Changes in Cash Balance from Budget and Other

Activities ............................................................................................................

58

Balance Sheets ...................................................................................................

59

Statements of Long-Term Fiscal Projections .....................................................

60

Statements of Social Insurance ..........................................................................

61

Statement of Changes in Social Insurance Amounts .........................................

64

Notes to the Financial Statements

Note 1. Summary of Significant Accounting Policies .......................................

66

Note 2. Cash and Other Monetary Assets ..........................................................

78

Note 3. Accounts and Taxes Receivable, Net ....................................................

80

Note 4. Loans Receivable and Loan Guarantee Liabilities, Net ........................

82

Note 5. Inventories and Related Property, Net ..................................................

85

Note 6. Property, Plant, and Equipment, Net .....................................................

86

Note 7. Debt and Equity Securities ....................................................................

87

Note 8. Investments in Government-Sponsored Enterprises .............................

90

Note 9. Other Assets ..........................................................................................

93

Note 10. Accounts Payable ................................................................................

94

Note 11. Federal Debt Securities Held by the Public and Accrued Interest ......

95

Note 12. Federal Employee and Veteran Benefits Payable ...............................

99

Note 13. Environmental and Disposal Liabilities ..............................................

109

Note 14. Benefits Due and Payable ...................................................................

111

Note 15. Insurance and Guarantee Program Liabilities .....................................

112

Note 16. Other Liabilities ..................................................................................

113

Note 17. Collections and Refunds of Federal Revenue .....................................

115

Note 18. Contingencies ......................................................................................

118

Note 19. Commitments ......................................................................................

123

Note 20. Funds from Dedicated Collections ......................................................

126

Note 21. Fiduciary Activities .............................................................................

132

Note 22. Social Insurance ..................................................................................

134

Note 23. Long-Term Fiscal Projections ............................................................

151

Note 24. Stewardship Land and Heritage Assets ...............................................

157

Note 25. Disclosure Entities and Related Parties ...............................................

158

Note 26. Subsequent Events .............................................................................

163

Required Supplementary Information (Unaudited)

The Sustainability of Fiscal Policy ....................................................................

164

Social Insurance .................................................................................................

175

Social Security and Medicare ..........................................................................

175

Railroad Retirement, Black Lung, and Unemployment Insurance ..................

198

Deferred Maintenance and Repairs ....................................................................

201

Other Claims for Refunds ..................................................................................

201

Tax Assessments ................................................................................................

202

Federal Oil and Gas Resources ..........................................................................

203

Federal Natural Resources Other than Oil and Gas ..........................................

205

Other Information (Unaudited)

Tax Burden .......................................................................................................

206

Tax Gap .............................................................................................................

207

Tax Expenditures ...............................................................................................

208

Unmatched Transactions and Balances .............................................................

210

Required Supplementary Stewardship Information (Unaudited)

Stewardship Investments ...................................................................................

212

Non-Federal Physical Property ........................................................................

213

Human Capital .................................................................................................

213

Research and Development .............................................................................

213

Appendices

Appendix A: Reporting Entity ...........................................................................

216

Appendix B: Acronyms .....................................................................................

220

U.S. Government Accountability Office Independent Auditor’s Report ......

226

This page is intentionally blank.

i Results in Brief – 2018 Financial Report of U.S. Government

RESULTS IN BRIEF

Highlights of the Fiscal Year 2018 Financial Report of the U.S.

Government

Where We Are Now

The government’s net cost before taxes

and other revenues for fiscal year 2018

was

$4.5 trillion - an increase of $10.1

billion (0.2 percent) from fiscal year

2017.

Net cost equals gross costs of

$4.8

trillion, less earned program revenues

(e.g., Medicare premiums, national

park entry fees), and then adjusted for

gains or losses from assumption

changes used to estimate future federal

employee and veterans benefits

payments.

The increase in net cost is the

combined effect of many offsetting

increases and decreases across the

government.

Total government tax and other

revenues grew by $9.7 billion (0.3

percent) to about $3.4 trillion for fiscal

year 2018.

The government deducts $3.4 trillion

in tax and other revenues from its $4.5

trillion net cost (with some

adjustments) to derive its fiscal year

2018 “bottom line” net operating cost

of $1.2 trillion, which is largely

unchanged compared to fiscal year

2017.

By comparison, the government’s

budget deficit for fiscal year 2018

was $779.0 billion – an increase of

$113.3 billion (about 17.0 percent) over fiscal year 2017. The $380.0 billion difference between the budget deficit

and net operating cost is primarily due to accrued costs (incurred but not necessarily paid) that are included in net

operating cost, but not the budget deficit. These include but are not limited to estimated future costs of federal

employee and veterans benefits.

Results in Brief – 2018 Financial Report of the U.S. Government ii

An Unsustainable Fiscal Path

The long-term fiscal projections indicate that the government’s debt-to-GDP ratio will rise from 78 percent in

2018 to 530 percent over the 75-year projection period, and will continue to rise thereafter, if current policy is

kept in place. The projections in this Financial Report show that current policy is not sustainable. These

projections assume that current policy will continue indefinitely, and are, therefore, neither forecasts nor

predictions. Nevertheless, policy changes must be enacted so that financial outcomes will be different than those

projected.

The primary deficit is the difference between non-interest spending and receipts. As a ratio relative to gross

domestic product (GDP), (the primary deficit-to-GDP ratio), it is useful for gauging long-term fiscal

sustainability. This ratio spiked from 2009 through 2012 due to the financial crisis of 2008-09, the ensuing severe

recession, and increased spending and temporary tax reductions enacted to stimulate the economy and support

recovery. As the economic recovery took hold, the primary deficit-to-GDP ratio fell, averaging 1.9 percent from

2013-2018. The ratio is projected to rise to 2.9 percent in 2019 and then shrink slightly through 2024 as the

economy grows. After 2024, increased spending for Social Security and health programs is projected to result in

increasing primary deficits that peak in 2039 at 4.1 percent. This is due to the continued retirement of the baby

boom generation and increases in health care costs. After 2039, the ratio gradually decreases to 2.5 percent in

2093 as the aging of the population slows. The primary deficit projections, along with those for interest rates and

GDP, determine the debt-to-GDP ratio projections.

These projections assume the individual income and estate and gift tax provisions of the TCJA are permanently

extended and discretionary spending grows at the same rate as nominal GDP beyond 2019. Congressional action

is required to make these changes. GDP, interest, and other economic and demographic assumptions are the same

as those that underlie the most recent Social Security and Medicare trustees’ report projections, adjusted for

historical revisions that occur annually. See Note 23 for more information.

If changes in policy are not so abrupt as to slow economic growth, then the sooner policy changes are adopted, the

smaller the changes to revenue and/or spending will be required to return the government to a sustainable fiscal

path.

1 Executive Summary to the 2018 Financial Report of U.S. Government

Executive Summary to the 2018 Financial Report of the U.S. Government 2

Executive Summary to the Fiscal Year 2018

Financial Report of the United States Government

The Fiscal Year 2018 Financial Report of the United States Government (Financial Report) presents the U.S.

government’s current financial position and condition, and discusses key financial topics and trends. The

Financial Report is produced by the U.S. Department of the Treasury (Treasury) in coordination with the Office

of Management and Budget (OMB) of the Executive Office of the President. The table on the preceding page

presents several key indicators of the government’s financial position and condition, which are discussed in this

Summary and, in greater detail, in the Financial Report. The Secretary of the Treasury, Director of OMB, and the

Comptroller General of the United States at the Government Accountability Office (GAO) believe that the

information discussed in this Financial Report is important to all Americans.

This Financial Report addresses the government’s financial activity and results as of and for the fiscal years

ended September 30, 2018 and 2017. Note 26, Subsequent Events discusses events that occurred after the end of

the fiscal year which may affect the government’s financial position and condition.

Where We Are Now

Comparing the Budget and the Financial Report

The Budget of the United States Government (Budget) and the Financial Report present complementary

perspectives on the government’s financial position and condition.

• The Budget is the government’s primary financial planning and control tool. It accounts for past government

receipts and spending, and includes the President’s proposed receipts and spending plan. Receipts are cash

received by the U.S. government and spending is measured as outlays, or payments made by the government

to the public. Receipts greater than outlays creates a budget surplus; and outlays greater than receipts creates a

budget deficit.

• The Financial Report includes the government’s costs and revenues, assets and liabilities, and other important

financial information. It compares the government’s revenues (amounts earned, but not necessarily collected),

with costs (amounts incurred, but not necessarily paid) to derive net operating cost.

Chart 1 compares the government’s budget deficit (receipts vs. outlays) and net operating cost (revenues vs.

costs) for fiscal years 2014 - 2018. During

fiscal year 2018:

• A $127.1 billion increase in outlays was

offset in part by a $13.8 billion increase in

receipts to increase the budget deficit by

$113.3 billion (about 17.0 percent) to

$779.0 billion.

• Net operating cost remained largely

unchanged during fiscal year 2018 at $1.2

trillion, increasing by $5.4 billion or 0.5

percent. This is due mostly to a $10.1

billion or 0.2 percent increase in net cost

which slightly more than offset a $9.7

billion or 0.3 percent increase in tax and

other revenues.

• The $380.0 billion difference between the

budget deficit and net operating cost is primarily due to accrued costs (incurred but not necessarily paid)

related to increases in estimated federal employee and veteran benefits liabilities and certain other liabilities

that are included in net operating cost, but not the budget deficit.

3 Executive Summary to the 2018 Financial Report of U.S. Government

Costs and Revenues

The government’s “bottom line” net operating cost remained largely unchanged at $1.2 trillion during fiscal year

2018, increasing by $5.4 billion (0.5 percent). It is calculated

as follows:

• Starting with total gross costs of $4.8 trillion, the

government subtracts earned program revenues (e.g.,

Medicare premiums, national park entry fees, and postal

service fees) and adjusts the balance for gains or losses

from changes in actuarial assumptions used to estimate

future federal employee and veterans benefits payments

to derive its net cost before taxes and other revenues of

$4.5 trillion (see Chart 2), an increase of $10.1 billion

(0.2 percent) from fiscal year 2017. This net increase is

the combined effect of many offsetting increases and

decreases across the government. For example:

o Entities administering federal employee and veterans

benefits programs, including the Office of Personnel Management (OPM), Department of Veterans Affairs

(VA), and Department of Defense (DOD) employ a complex series of assumptions, including but not limited

to interest rates, beneficiary eligibility, life expectancy, and medical cost levels, to make actuarial projections

of their long-term benefits liabilities. Changes in these assumptions can result in either losses (net cost

increases) or gains (net cost decreases). Across the government, these net losses from changes in assumptions

amounted to $125.2 billion in fiscal year 2018, a loss decrease (and a corresponding net cost decrease) of

$231.3 billion compared to fiscal year 2017.

o The Department of Energy’s (DOE) net cost increased by $99.6 billion, predominantly due changes in

estimated environmental remediation costs.

o Department of Health and Human Services (HHS) and Social Security Administration (SSA) net costs

increased $56.4 billion and $39.5 billion, respectively, largely due to increases in benefit expenses from the

social insurance programs administered by those entities (e.g., Medicare, Social Security).

o

At DOD, a $33.0 billion net cost increase includes a $39.2 billion decrease in earned revenues across the

Department, as well as increases in the costs of procurement, personnel, and research and development.

These increases were partially offset by a decrease in losses from changes in assumptions referenced

above and a decrease in costs of military operations, readiness, and support.

o Interest costs related to the federal debt held by the public increased by $61.0 billion due largely to an increase

in the debt and average interest rates, as well as inflation adjustments on certain Treasury securities. Interest

costs increased by 20.6 percent in 2018 from 2017 and by 37.4 percent over the past five years.

• The government deducts tax and other revenues from net cost (with some adjustments) to derive its fiscal year

2018 “bottom line” net operating cost of $1.2 trillion.

o From Chart 3, total government tax and other

revenues grew by $9.7 billion (0.3 percent) to about

$3.4 trillion for fiscal year 2018.

o Together, individual income tax and tax

withholdings, and corporate taxes accounted for

about 88.7 percent of total tax and other revenues in

fiscal year 2018. Other revenues include Federal

Reserve earnings, excise taxes, and customs duties.

Executive Summary to the 2018 Financial Report of the U.S. Government 4

Assets and Liabilities

Chart 4 summarizes the assets and liabilities that the government reports on its Balance Sheet. As of

September 30, 2018:

• Total assets ($3.8 trillion) consist mostly

of $1.4 trillion in net loans receivable

(primarily student loans) and $1.1 trillion

in net property, plant, and equipment).

o Other significant government

resources not reported on the Balance

Sheet include stewardship assets,

natural resources, and the

government’s power to tax and set

monetary policy.

• Total liabilities ($25.4 trillion) consist

mostly of: (1) $15.8 trillion in federal debt

securities held by the public and accrued

interest and (2) $8.0 trillion in federal

employee and veteran benefits payable.

o The “public” consists of individuals, corporations, state and local governments, Federal Reserve Banks,

foreign governments, and other entities outside the federal government.

• The government also reports about $5.8 trillion of intragovernmental debt outstanding, which arises when one

part of the government borrows from another.

o For example, government funds (e.g., Social Security and Medicare trust funds) typically must invest

excess annual receipts, including interest earnings, in Treasury-issued federal debt securities. Although

not reflected in Chart 4, these securities are included in the calculation of federal debt subject to the debt

limit.

• Debt held by the public plus intragovernmental debt equals gross federal debt, which, with some adjustments,

is subject to a statutory debt ceiling (“debt limit”).

o At the end of fiscal year 2018, debt subject to the statutory limit was $21.5 trillion. Increasing or

suspending the debt limit does not increase spending or authorize new spending; rather, it permits the

government to continue to honor pre-existing commitments.

o Legislation most recently suspended the debt limit from February 9, 2018 through March 1, 2019.

Effective March 2, 2019, the statutory debt limit was set at $22.0 trillion, and on March 4, 2019, the

Secretary of the Treasury notified the Congress that the statutory debt limit would be reached on or after

that day. When delays in raising the debt limit occur, Treasury implements “extraordinary measures” on

a temporary basis, to enable the government to protect the full faith and credit of the United States by

continuing to pay its bills. Treasury began taking these extraordinary measures on March 4, 2019.

Key Economic Trends

An examination of key macroeconomic indicators is essential to the discussion of the government’s financial

performance. During fiscal year 2018, economic growth and the pace of job creation each accelerated, and the

unemployment rate declined to a 49-year low. These and other economic and financial developments are

discussed in greater detail in the Financial Report.

5 Executive Summary to the 2018 Financial Report of U.S. Government

An Unsustainable Fiscal Path

An important purpose of this Financial Report is to help citizens understand current fiscal policy and the

importance and magnitude of policy reforms necessary to make it sustainable. A sustainable fiscal policy is one

where the ratio of debt held by the public to GDP (the debt-to-GDP ratio) is stable or declining over the long

term. GDP measures the size of the nation’s economy in terms of the total value of all final goods and services

that are produced in a year. Considering financial results relative to GDP is a useful indicator of the economy’s

capacity to sustain the government’s many programs.

The current fiscal path is unsustainable. To determine if current fiscal policy is sustainable, the projections

discussed in the Financial Report assume current policy will continue indefinitely.

1

The projections are therefore

neither forecasts nor predictions. Nevertheless, policy changes must be enacted so that actual financial outcomes

will be different than those projected.

Receipts, Spending, and the Debt

Chart 5 shows historical and current policy projections for receipts, non-interest spending by major category,

net interest, and total spending expressed

as a percent of GDP.

• The primary deficit is the difference

between non-interest spending and

receipts. The primary deficit

expressed as a ratio relative to GDP

(the primary deficit-to-GDP ratio) is

useful for gauging long-term fiscal

sustainability.

• The primary deficit-to-GDP ratio

spiked during 2009 through 2012 due

to the financial crisis of 2008-09 and

the ensuing severe recession, as well

as increased spending and temporary

tax reductions enacted to stimulate the

economy and support recovery. As an

economic recovery took hold, the

primary deficit-to-GDP ratio fell,

averaging 1.9 percent from 2013-2018. The ratio is projected to rise to 2.9 percent in 2019 and then shrink

slightly through 2024 as the economy grows. After 2024, however, increased spending for Social Security and

health programs

2

due to the continued retirement of the baby boom generation and increases in health care

costs is projected to result in increasing primary deficits that peak in 2039, when the primary deficit-to-GDP

ratio reaches 4.1 percent. After 2039, the ratio gradually decreases as the aging of the population continues at

a slower pace, and reaches 2.5 percent in 2093.

• These projections assume the individual income and estate and gift tax provisions of the TCJA are

permanently extended and discretionary spending grows at the same rate as nominal GDP beyond 2019.

Congressional action is required to make these changes. GDP, interest, and other economic and demographic

assumptions are the same as those that underlie the most recent Social Security and Medicare trustees’ report

projections, adjusted for historical revisions that occur annually. See Note 23 for more information.

1

Current policy in the projections is based on current law, but includes extension of certain policies that expire under current law but are routinely extended

or otherwise expected to continue.

2

See the 2018 Trustees Report for Medicare (pp 4-5) and Social Security (pp 4-23) and the 2017 Medicaid Actuarial Report

Executive Summary to the 2018 Financial Report of the U.S. Government 6

• The persistent long-term gap between projected receipts and total spending shown in Chart 5 occurs despite

the projected effects of the Affordable Care Act (ACA)

3

on long-term deficits.

o Enactment of the ACA in 2010 and the Medicare Access and CHIP Reauthorization Act (MACRA) in

2015 established cost controls for Medicare hospital and physician payments whose long-term

effectiveness is still to be demonstrated.

o There is uncertainty about the extent to which these projections can be achieved and whether the

ACA’s provisions that reduce Medicare cost growth will be overridden by new legislation.

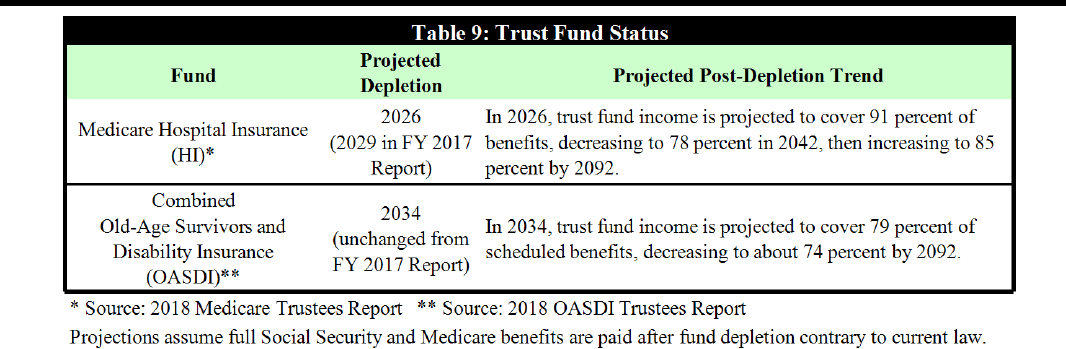

Table 1 summarizes the status and projected trends of the government’s Social Security and Medicare Trust

Funds.

The primary deficit projections in Chart 5, along with those for interest rates and GDP, determine the debt-

to-GDP ratio projections in Chart 6.

• The debt-to-GDP ratio was 78 percent

at the end of fiscal year 2018, and

under current policy is projected to

exceed 100 percent by 2030, and

reach 530 percent in 2093.

• The debt-to-GDP ratio rises

continuously mainly because higher

levels of debt lead to higher net

interest expenditures, which lead to

higher deficits and debt. The

continuous rise of the debt-to-GDP

ratio indicates that current fiscal

policy is unsustainable.

• These debt-to-GDP projections are

higher than the corresponding

projections in both the fiscal year

2017 and fiscal year 2016 Financial Reports.

3

The ACA refers to P.L. 111-148, as amended by P.L. 111-152. The ACA expands health insurance coverage, provides health insurance subsidies for low-

income individuals and families, includes many measures designed to reduce health care cost growth, and significantly reduces Medicare payment rates

relative to the rates that would have occurred in the absence of the ACA. (See Note 22 and the Required Supplementary Information section of the Financial

Report, and the 2018 Medicare Trustees Report for more information).

7 Executive Summary to the 2018 Financial Report of U.S. Government

The Fiscal Gap and the Cost of Delaying Fiscal Policy Reform

• The 75-year fiscal gap is a measure of how much primary deficits must be reduced over the next 75 years in

order to make fiscal policy sustainable. That estimated fiscal gap for 2018 is 4.1 percent of GDP (compared to

2.0 percent for 2017).

• This estimate implies that making fiscal policy sustainable over the next 75 years would require some

combination of spending reductions and receipt increases that equals 4.1 percent of GDP on average over the

next 75 years. The fiscal gap represents 21.9 percent of 75-year present value receipts and 18.6 percent of 75-

year present value non-interest spending.

• The timing of policy changes to make fiscal policy sustainable has important implications for the well-being

of future generations as is shown in Table 2.

o Table 2 shows that, if action is delayed by 10 years, the estimated magnitude of primary surplus

increases necessary to close the 75-year fiscal gap increases by nearly 20 percent from 4.1 percent of

GDP on average over 75 years to 4.9 percent on average over 65 years); if action is delayed by 20

years, the magnitude of reforms necessary increases by about 46 percent.

o Future generations are harmed by a policy delay because the higher the primary surpluses are during

their lifetimes, the greater is the difference between the taxes they pay and the programmatic

spending from which they benefit.

Conclusion

• Projections in the Financial Report indicate that the government’s debt-to-GDP ratio is projected to rise over

the 75-year projection period and beyond if current policy is kept in place. The projections in this Financial

Report show that current policy is not sustainable.

• If changes in fiscal policy are not so abrupt as to slow economic growth and the sooner those policy changes

are adopted, the smaller the changes to revenue and/or spending will be required to return the government to a

sustainable fiscal path.

Find Out More

The 2018 Financial Report and other information about the nation’s finances are available at:

• U.S. Department of the Treasury,

http://www.fiscal.treasury.gov/fsreports/rpt/finrep/fr/fr_index.htm;

• OMB’s Office of Federal Financial Management, https://www.whitehouse.gov/omb/management/office-federal-

financial-management/; and

• GAO, http://www.gao.gov/financial.html

The Government Accountability Office’s (GAO) audit report on the U.S. government’s consolidated financial

statements can be found beginning on page 226 of the full Financial Report. GAO was unable to express an

opinion (disclaimed) on these consolidated financial statements for the reasons discussed in the audit report.

MANAGEMENT’S DISCUSSION AND ANALYSIS

8

MANAGEMENT’S DISCUSSION AND

ANALYSIS

Introduction

The Fiscal Year 2018 Financial Report of the United States Government (Financial Report) provides the President,

Congress, and the American people with a comprehensive view of the federal government’s financial position and condition,

and discusses important financial issues and significant conditions that may affect future operations, including the need to

achieve fiscal sustainability over the medium and long term.

Pursuant to 31 United States Code (U.S.C.) § 331(e)(1), the Department of the Treasury (Treasury), in cooperation with

the Office of Management and Budget (OMB), must submit an audited (by the Government Accountability Office or GAO)

financial statement for the preceding fiscal year, covering all accounts and associated activities of the executive branch of the

United States (U.S.) government

1

to the President and Congress no later than six months after the September 30 fiscal year-

end.

The Financial Report is prepared from the financial information provided by 158 federal consolidation entities (see

organizational chart on the next page and Appendix A). As it has for the past 21 years, GAO issued a disclaimer of opinion

on the accrual-based, consolidated financial statements for the fiscal years ended September 30, 2018 and 2017. GAO also

issued a disclaimer of opinion on the sustainability financial statements, which consist of the 2018 and 2017 Statements of

Long-Term Fiscal Projections (SLTFP); the 2018, 2017, 2016, 2015, and 2014 Statements of Social Insurance (SOSI); and

the 2018 and 2017 Statements of Changes in Social Insurance Amounts (SCSIA). A disclaimer of opinion indicates that

sufficient information was not available for the auditors to determine whether the reported financial statements were fairly

presented in accordance with U.S. Generally Accepted Accounting Principles (GAAP). In fiscal year 2018, 35

2

of the 40

most significant entities earned unmodified (“clean”) opinions on their financial statements.

The fiscal year 2018 Financial Report consists of:

• Management’s Discussion and Analysis (MD&A), which provides management’s perspectives on and analysis

of information presented in the Financial Report, such as financial and performance trends;

• Principal financial statements and the related notes to the financial statements;

• Required Supplementary Information (RSI), Required Supplementary Stewardship Information (RSSI), and

Other Information; and

• GAO’s audit report.

This Financial Report addresses the government’s financial activity and results as of and for the fiscal years ended

September 30, 2018 and 2017. Note 26, Subsequent Events discusses events that occurred after the end of the fiscal year

which may affect the government’s financial position and condition.

In addition, the Results in Brief and Executive Summary to this Financial Report provides a quick reference to the key

issues in the Financial Report and an overview of the government's financial position and condition.

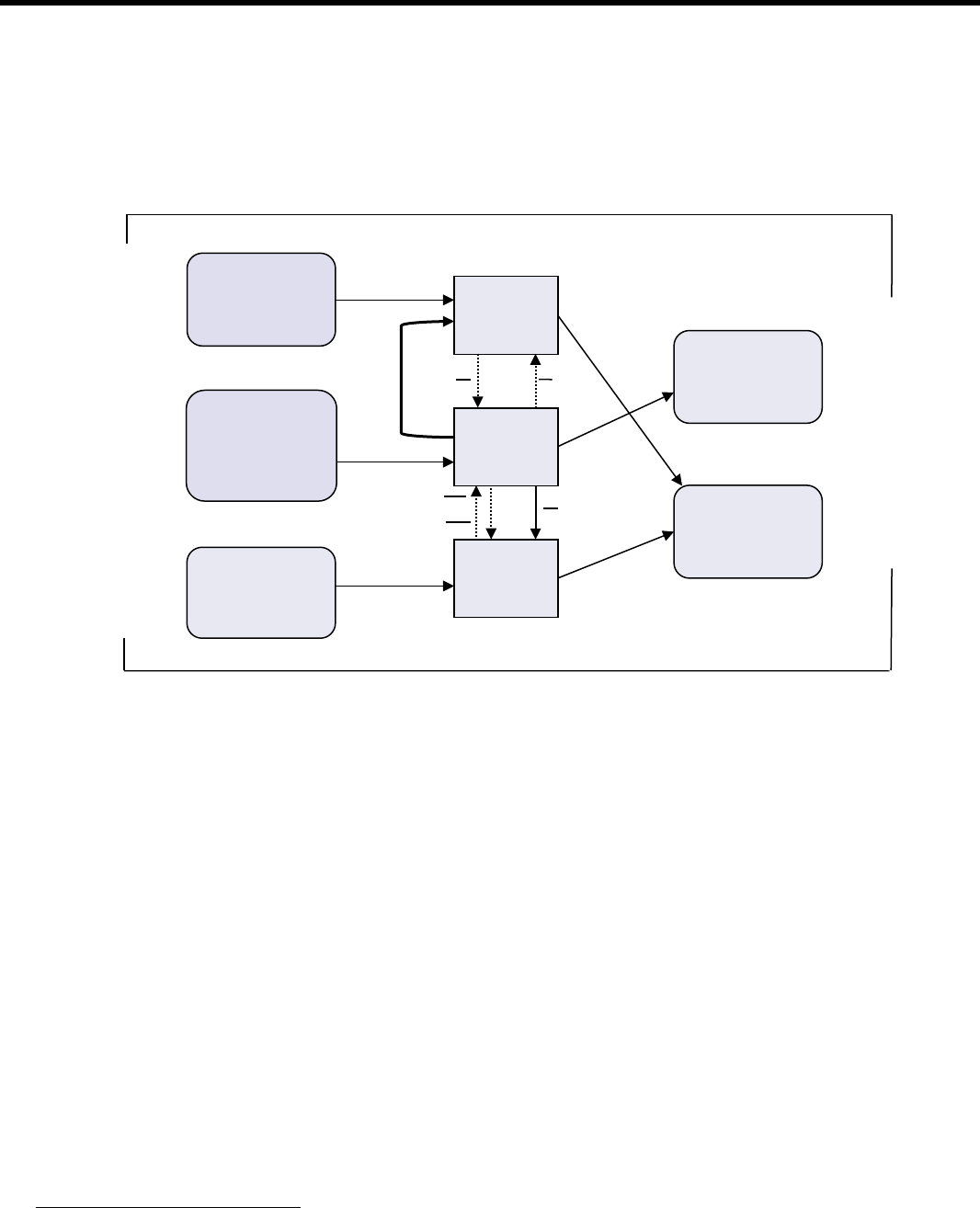

Mission & Organization

The government’s fundamental mission is derived from the Constitution: “…to form a more perfect union, establish

justice, insure domestic tranquility, provide for the common defense, promote the general welfare and secure the blessings of

liberty to ourselves and our posterity.” The government’s functions have evolved over time to include health care, income

security, veterans benefits and services, housing and transportation, security, and education. Exhibit 1 provides an overview

of how the U.S. government is organized.

1

The Government Management Reform Act of 1994 has required such reporting, covering the executive branch of the Government, beginning with financial

statements prepared for fiscal year 1997. The consolidated financial statements include the legislative and judicial branches.

2

The 35 entities include the Department of Health and Human Services, which received disclaimers of opinion on its 2018, 2017, 2016, 2015, and 2014

SOSI and on its 2018 and 2017 SCSIA.

9

MANAGEMENT’S DISCUSSION AND ANALYSIS

Exhibit 1

THE UNITED STATES GOVERNMENT

EXECUTIVE BRANCH

THE PRESIDENT

THE VICE PRESIDENT

EXECUTIVE OFFICE OF THE PRESIDENT

White House Office

Office of the Vice President

Council of Economic Advisers

Council on Environmental Quality

National Security Council

Office of Administration

Office of Management and Budget

Office of National Drug Control Policy

Office of Policy Development

Office of Science and Technology Policy

Office of the U.S. Trade Representative

LEGISLATIVE BRANCH

THE CONGRESS

SENATE HOUSE

Architect of the Capitol

U.S. Botanic Garden

Government Accountability Office

Government Publishing Office

Library of Congress

Congressional Budget Office

U.S. Capitol Police

JUDICIAL BRANCH

THE SUPREME COURT

OF THE U.S.

U.S. Courts of Appeals

U.S. District Courts

Territorial Courts

U.S. Court of International Trade

U.S. Court of Federal Claims

Administrative Office of the U.S. Courts

Federal Judicial Center

U.S. Sentencing Commission

OTHER SIGNIFICANT CONSOLIDATION ENTITIES

ENVIRONMENTAL PROTECTION AGENCY

FEDERAL COMMUNICATIONS COMMISSION

GENERAL SERVICES ADMINISTRATION

FEDERAL DEPOSIT INSURANCE CORPORATION

NATIONAL AERONAUTICS AND SPACE ADMINISTRATION

GENERAL FUND OF THE U.S. GOVERNMENT

NATIONAL SCIENCE FOUNDATION

MILLENNIUM CHALLENGE CORPORATION

OFFICE OF PERSONNEL MANAGEMENT

NATIONAL CREDIT UNION ADMINISTRATION

SMALL BUSINESS ADMINISTRATION

NATIONAL RAILROAD RETIREMENT INVESTMENT TRUST

SOCIAL SECURITY ADMINISTRATION

OVERSEAS PRIVATE INVESTMENT CORPORATION

U.S. AGENCY FOR INTERNATIONAL DEVELOPMENT

PENSION BENEFIT GUARANTY CORPORATION

U.S. NUCLEAR REGULATORY COMMISSION

RAILROAD RETIREMENT BOARD

SECURITY ASSISTANCE ACCOUNTS

SECURITIES AND EXCHANGE COMMISSION

EXPORT-IMPORT BANK OF THE U.S.

SMITHSONIAN INSTITUTION

FARM CREDIT SYSTEM INSURANCE CORPORATION

TENNESSEE VALLEY AUTHORITY

U.S. POSTAL SERVICE

OTHER CONSOLIDATION ENTITIES ARE LISTED IN APPENDIX A OF THIS FINANCIAL REPORT

DEPARTMENT

OF

VETERANS

AFFAIRS

DEPARTMENT

OF THE

TREASURY

DEPARTMENT

OF

TRANSPORTATION

DEPARTMENT

OF

STATE

DEPARTMENT

OF

LABOR

DEPARTMENT

OF HOUSING

AND URBAN

DEVELOPMENT

DEPARTMENT

OF THE

INTERIOR

DEPARTMENT

OF

JUSTICE

DEPARTMENT

OF HOMELAND

SECURITY

DEPARTMENT

OF HEALTH

AND HUMAN

SERVICES

DEPARTMENT

OF

DEFENSE

DEPARTMENT

OF

EDUCATION

DEPARTMENT

OF

ENERGY

DEPARTMENT

OF

COMMERCE

DEPARTMENT

OF

AGRICULTURE

SIGNIFICANT CONSOLIDATION ENTITIES

THE CONSTITUTION

MANAGEMENT’S DISCUSSION AND ANALYSIS

10

The Government’s Financial Position and Condition

This Financial Report presents the government’s financial position at the end of the fiscal year, explains how and why

the financial position changed during the year, and discusses the government’s financial condition and how it may change in

the future.

11

MANAGEMENT’S DISCUSSION AND ANALYSIS

Table 1 on the previous page and the following summarize the federal government’s financial position:

• During fiscal year 2018, the budget deficit increased by 17.0 percent and gross cost increased by 4.4 percent, while

net cost, tax and other revenues, and net operating cost each increased by less than one percent.

• The government’s gross costs of $4.8 trillion, less $392.8 billion in revenues earned for goods and services provided

to the public (e.g., Medicare premiums, national park entry fees, and postal service fees), plus $125.2 billion in net

losses from changes in assumptions (e.g., interest rates, inflation, disability claims rates) yields the government’s net

cost of $4.5 trillion, a slight increase of $10.1 billion or 0.2 percent over fiscal year 2017.

• Deducting $3.4 trillion in tax and other revenues, with some adjustment for unmatched transactions and balances,

results in a “bottom line” net operating cost of $1.2 trillion for fiscal year 2018, an increase of $5.4 billion or 0.5

percent over fiscal year 2017.

• Comparing total 2018 government assets of $3.8 trillion to total liabilities of $25.4 trillion (comprised mostly of

$15.8 trillion in federal debt held by the public and accrued interest payable

3

, and $8.0 trillion of federal employee

and veterans benefits payable) yields a negative net position of $21.5 trillion.

• The budget deficit is primarily financed through borrowing from the public. As of September 30, 2018, debt held by

the public, excluding accrued interest, was $15.8 trillion. This amount, plus intragovernmental debt ($5.8 trillion)

equals gross federal debt, which, with some adjustments, is subject to the statutory debt limit. As of September 30,

2018, the government’s total debt subject to the debt limit was $21.5 trillion. The statutory debt limit was most

recently suspended through March 1, 2019.

This Financial Report also contains information about projected impacts on the government’s future financial condition.

Under federal accounting rules, social insurance amounts as reported in both the SLTFP and in the SOSI are not considered

liabilities of the government. From Table 1:

• The SLTFP shows that the present value (PV)

4

of total non-interest spending, including Social Security, Medicare,

Medicaid, defense, and education, etc.), over the next 75 years, under current policy, is projected to exceed the PV

of total receipts by $46.2 trillion (total federal non-interest net expenditures from Table 1).

• The SOSI shows that the PV of the government’s expenditures for Social Security and Medicare Parts A, B and D,

and other social insurance programs over 75 years is projected to exceed social insurance revenues

5

by about $53.8

trillion, a $4.8 trillion increase over 2017 social insurance projections.

• The two sustainability measures in Table 1 differ primarily because total non-interest net expenditures from the

SLTFP include the effects of general revenues and non-social insurance spending, neither of which is included in the

SOSI.

The government’s current financial position and long-term financial condition can be evaluated both in dollar terms and

in relation to the economy as a whole. Gross Domestic Product (GDP) is a measure of the size of the nation’s economy in

terms of the total value of all final goods and services that are produced in a year. Considering financial results relative to

GDP is a useful indicator of the economy’s capacity to sustain the government’s many programs. For example:

• The budget deficit (i.e., including the consolidated receipts and outlays from federal funds and the Social Security

Trust Fund) increased from $665.7 billion in fiscal year 2017 to $779.0 billion in fiscal year 2018. The deficit-to-

GDP ratio in 2018 was 3.9 percent, an increase from 3.5 percent in fiscal year 2017 and above the 3.2 percent

average over the past 40 years.

6

• The budget deficit is primarily financed through borrowing from the public. As of September 30, 2018, the $15.8

trillion in debt held by the public, excluding accrued interest, equates to approximately 78 percent of GDP.

• The 2018 SOSI projection of $53.8 trillion net PV excess of expenditures over receipts over 75 years represents

about 4.0 percent of the PV of GDP over 75 years. The excess of total projected non-interest spending over receipts

of $46.2 trillion from the SLTFP represents 3.3 percent of GDP over 75 years. As discussed in this Financial

Report, changes in these projections can, in turn, have a significant impact on projected debt as a percent of GDP.

• To prevent the debt-to-GDP ratio from rising over the next 75 years, a combination of non-interest spending

reductions and receipts increases that amounts to 4.1 percent of GDP on average is needed (2.0 percent of GDP on

average in the 2017 projections). The fiscal gap represents 21.9 percent of 75-year present value receipts and 18.6

percent of 75-year present value non-interest spending.

3

On the government’s Balance Sheet, debt held by the public and accrued interest payable consists of Treasury securities, net of unamortized discounts and

premiums, and accrued interest payable. The “public” consists of individuals, corporations, state and local governments, Federal Reserve Banks, foreign

governments, and other entities outside the federal government.

4

Present values recognize that a dollar paid or collected in the future is worth less than a dollar today because a dollar today could be invested and earn

interest. To calculate a present value, future amounts are thus reduced using an assumed interest rate, and those reduced amounts are summed.

5

Social Security is funded by the payroll taxes and revenue from taxation of benefits. Medicare Part A is funded by the payroll taxes, revenue from taxation

of benefits, and premiums that support those programs. Medicare Parts B and D are primarily financed by general revenues and premiums. By accounting

convention, these general revenues are eliminated in consolidation at the governmentwide level and, as such, are not included in the SOSI. For the fiscal year

2018 and 2017 SOSI, the amounts eliminated totaled $32.9 trillion and $30.0 trillion, respectively.

6

Final Monthly Treasury Statement (as of September 30, 2018 and 2017), Joint Statement of Treasury Secretary Steven T. Mnuchin and OMB Director

Mick Mulvaney on Budget Results for Fiscal Year 2018

MANAGEMENT’S DISCUSSION AND ANALYSIS

12

Fiscal Year 2018 Financial Statement Audit Results

For fiscal year 2018, GAO issued a disclaimer of audit opinion on the accrual-based, governmentwide financial

statements, as it has for the past 21 years, due to certain material weaknesses in internal control over financial reporting and

other limitations on the scope of its work. In addition, GAO issued a disclaimer of opinion on the sustainability financial

statements due to significant uncertainties primarily related to the achievement of projected reductions in Medicare cost

growth and certain other limitations. GAO’s audit report on page 226 of this Financial Report, discusses GAO’s findings.

22 of the 24 entities required to issue audited financial statements under the Chief Financial Officers (CFO) Act

received unmodified audit opinions, as did 13 of 16 additional significant reporting entities (see Table 10 and Appendix A).

7

The Governmentwide Reporting Entity

This Financial Report includes the financial status and activities of the executive, legislative, and judicial branches of

the federal government. Statement of Federal Financial Accounting Standards (SFFAS) No. 47, Reporting Entity, provides

criteria for identifying organizations that are consolidation entities, disclosure entities, and related parties. Such criteria are

summarized in Note 1A and in Appendix A, which lists the entities included in this Financial Report by these categories. The

assets, liabilities, results of operations, and related activity for consolidation entities are consolidated in the financial

statements.

The Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie

Mac) meet the criteria for disclosure entities and, consequently, are not consolidated into the government’s financial

statements. However, the values of the investments in such entities, changes in value, and related activity with these entities

are included in the consolidated financial statements. The Federal Reserve System (FR System) is a disclosure entity and is

not consolidated into the government’s financial statements. See Note 1A—Significant Accounting Policies, Reporting Entity

and Note 25—Disclosure Entities and Related Parties for additional information. In addition, per SFFAS No. 31, Accounting

for Fiduciary Activities, fiduciary funds are not consolidated in the government financial statements.

8

Most significant reporting entities prepare financial reports that include financial and performance related information,

as well as Annual Performance Reports. More information may be obtained from entities’ websites indicated in Appendix A

and at www.performance.gov

.

The following pages contain a more detailed discussion of the government’s financial results for fiscal year 2018, the

budget, the economy, the debt, and a long-term perspective about fiscal sustainability, including the government’s ability to

meet its social insurance benefits obligations. The information in this Financial Report, when combined with the Budget of

the U.S. Government (Budget), collectively presents information on the government’s financial position and condition.

Accounting Differences Between the Budget and the Financial

Report

Each year, the Administration issues two reports that detail the government’s financial results: the Budget and this

Financial Report. The exhibit on the following page provides the key characteristics and differences between the two

documents.

Treasury generally prepares the financial statements in this Financial Report on an accrual basis of accounting as

prescribed by GAAP for federal entities.

9

These principles are tailored to the government’s unique characteristics and

circumstances. For example, entities prepare a uniquely structured “Statement of Net Cost,” which is intended to present net

government resources used in its operations. Also, unique to government is the preparation of separate statements to

reconcile differences and articulate the relationship between the budget and financial accounting results.

7

The 22 entities include the Department of Health and Human Services, which received disclaimers of opinions on its 2018, 2017, 2016, 2015, and 2014,

SOSI and its 2018 and 2017 SCSIA. The 13 entities include the Federal Deposit Insurance Corporation (FDIC), the National Credit Union Administration

(NCUA), and the Farm Credit System Insurance Corporation (FCSIC), which operate on a calendar year basis (December 31 year-end). Statistic reflects

2017 audit results for these organizations if 2018 results are not available.

8

See Note 21—Fiduciary Activities

9

Under GAAP, most U.S. government revenues are recognized on a ‘modified cash’ basis, (see Financial Statement Note 1.B). The Statement of Social

Insurance presents the present value of the estimated future revenues and expenditures for scheduled benefits over the next 75 years for the Social Security,

Medicare, Railroad Retirement programs; and 25 years for the Black Lung program. The Statement of Long-Term Fiscal Projections presents the present

value of the projected future receipts and non-interest spending for the federal government.

13

MANAGEMENT’S DISCUSSION AND ANALYSIS

Budget of the U.S. Government

Financial Report of the U.S. Government

Prepared primarily on a “cash basis”

• Initiative-

based and prospective: focus on

current and future initiatives planned and

how resources will be used to fund them.

•

Receipts (“cash in”), taxes and other

collections recorded when received.

• Outlays (“cash out”), largely recorded when

payment is made.

Prepared on an “accrual and modified cash basis”

• Entity-based and retrospective –

prior and present

resources used to implement initiatives.

•

Revenue: Tax revenue (more than 90 percent of total

revenue) recognized on modified cash basis (see Financial

Statement Note 1.B). Remainder recognized when earned,

but not necessarily received.

• Costs: recognized when incurred, but not necessarily paid.

Budget Deficit vs. Net Operating Cost

The budget deficit is measured as the excess of outlays, or payments made by the government, over receipts, or cash

received by the government. Net operating cost, on an accrual basis, is the excess of costs (what the government has incurred,

but has not necessarily paid) over revenues (what the government has collected and expects to collect, but has not necessarily

received). As shown in Chart A, net operating cost typically exceeds the budget deficit due largely to the inclusion of cost

accruals associated with increases in estimated liabilities for the government’s postemployment benefit programs for its

military and civilian employees and veterans as well as environmental liabilities.

The government’s primarily cash-based

10

budget deficit increased by $113.3 billion (about 17.0 percent) from

approximately $665.7 billion in fiscal year 2017 to about $779.0 billion in fiscal year 2018 due to lower growth in receipts

compared to the increase in outlays in fiscal year 2018. The $13.8 billion (0.4 percent) increase in receipts can be attributed

primarily to higher net individual income tax receipts, excise taxes, social insurance and retirement receipts, and customs

duties. Outlays increased $127.1 billion (3.2 percent). Contributing to the increase over fiscal year 2017 were higher outlays

for Defense, Medicaid, Social Security, disaster relief and flood insurance, Refundable Premium Tax Credits and cost sharing

reductions, interest on the Treasury debt held by the public (public debt), and lower government-sponsored enterprises’

(GSE) receipts (i.e., dividends from Fannie Mae and Freddie Mac), which are an offset to outlays.

11

The Treasury Department’s September 2018 Monthly Treasury Statement (MTS) is the source of receipts, spending,

and deficit information for this Report. The MTS presents primarily cash-based spending, or outlays, for the fiscal year in a

number of ways, including by month, by entity, and by budget function classification. The federal budget is divided into

approximately 20 categories – or budget functions - as a means of organizing federal spending by primary purpose (e.g.,

National Defense, Transportation, Health). Multiple entities may contribute to one or more budget functions, and a single

10

Interest outlays on Treasury debt held by the public are recorded in the budget when interest accrues, not when the interest payment is made. For federal

credit programs, outlays are recorded when loans are disbursed, in an amount representing the present value cost to the government, commonly referred to as

credit subsidy cost. Credit subsidy cost excludes administrative costs.

11

10/15/18 press release -- Joint Statement of Treasury Secretary Steven T. Mnuchin and OMB Director Mick Mulvaney on Budget Results for Fiscal Year

2018.

MANAGEMENT’S DISCUSSION AND ANALYSIS

14

budget function may be associated with only one entity. For example, the Department of Defense (DOD), Department of

Homeland Security (DHS), the Department of Energy (DOE), and multiple other entities administer programs that are critical

to the broader functional classification of National Defense. DOD, the Office of Personnel Management (OPM), and many

other entities also administer Income Security programs (e.g., retirement benefits, housing, financial assistance). By

comparison, the Medicare program is a budget function category unto itself and is administered exclusively at the federal

level by the Department of Health and Human Services (HHS). Federal spending information by budget function and other

categorizations may be found in the September 2018 MTS.

12

The government’s largely accrual-based net operating cost remained largely unchanged at $1.2 trillion increasing by

$5.4 billion (0.5 percent) during fiscal year 2018. As explained below, net operating costs are affected by both changes in

revenues and costs.

Table 2 provides a summary of the items reported in the Reconciliation of Net Operating Cost and Budget Deficit,

which articulates the relationship between the government’s accrual-based net operating cost and the primarily cash-based

budget deficit. From Table 2, the $380.0 billion net difference between the government’s budget deficit and net operating

cost for fiscal year 2018, is mostly attributable to: (1) a $282.2 billion net increase in liabilities for federal employee and

veteran benefits payable, (2) a $112.8 billion increase in environmental and disposal liabilities; and (3) several offsetting

items, including, but not limited to a $32.3 billion decrease in insurance and guarantee program liabilities and a $15.9 billion

increase in Accounts Payable. These affect net operating cost, but not the budget deficit.

12

Final Monthly Treasury Statement for Fiscal Year 2018 through September 30, 2018 and Other Periods.

15

MANAGEMENT’S DISCUSSION AND ANALYSIS

The Government’s Net Position: “Where We Are”

The government’s financial position and condition have traditionally been expressed through the Budget, focusing on

surpluses, deficits, and debt. However, this primarily cash-based discussion of the government’s net outlays (deficit) or net

receipts (surplus) tells only part of the story. The government’s accrual-based net position, (the difference between its assets

and liabilities), and its “bottom line” net operating cost (the difference between its revenues and costs) are also key financial

indicators.

Costs and Revenues

The government’s Statement of Operations and Changes in Net Position, much like a corporation’s income statement,

shows the government’s “bottom line” and its impact on net position (i.e., assets net of liabilities). To derive the

government’s “bottom line” net operating cost, the Statement of Net Cost first shows how much it costs to operate the federal

government, recognizing expenses when incurred, regardless of when payment is made (accrual basis). It shows the

derivation of the government’s net cost or the net of: (1) gross costs, or the costs of goods produced and services rendered by

the government, (2) the earned revenues generated by those goods and services during the fiscal year, and (3) gains or losses

from changes in actuarial assumptions used to estimate certain liabilities. This amount, in turn, is offset against the

government’s taxes and other revenue reported in the Statement of Operations and Changes in Net Position to calculate the

“bottom line” or net operating cost.

13

Table 3 shows that the government’s “bottom line” net operating cost remained largely unchanged during 2018 at $1.2

trillion increasing only $5.4 billion (0.5 percent), during the fiscal year. This slight increase is due mostly to a $10.1 billion

(0.2 percent) increase in entity net costs, which slightly more than offset a $9.7 billion (0.3 percent) increase in tax and other

revenues over the past fiscal year as discussed in the following.

Gross Cost and Net Cost

The Statement of Net Cost starts with the government’s total gross costs of $4.8 trillion, subtracts revenues earned for

goods and services provided (e.g., Medicare premiums, national park entry fees, and postal service fees), and adjusts the

balance for gains or losses from changes in actuarial assumptions used to estimate certain liabilities, including federal

employee and veterans benefits to derive its net cost of $4.5 trillion (See Chart C), a $10.1 billion (0.2 percent) increase over

fiscal year 2017.

Typically, the annual change in the government’s net cost is impacted by a variety of offsetting increases and decreases

across entities. For example, offsetting changes in net cost during fiscal year 2018 included:

• Entities administering federal employee and veterans benefits programs employ a complex series of assumptions,

including but not limited to interest rates, beneficiary eligibility, life expectancy, and medical cost levels, to make

actuarial projections of their long-term benefits liabilities. Changes in these assumptions can result in either losses

(net cost increases) or gains (net cost decreases). Across the government, these net losses from changes in

assumptions amounted to $125.2 billion in fiscal year 2018, a loss decrease (and a corresponding net cost decrease)

of $231.3 billion compared to fiscal year 2017. The primary entities that administer programs impacted by these

assumptions – typically federal employee pension and benefit programs – are the OPM,

Department of Veterans

Affairs (VA), and DOD. These entities recorded losses from changes in assumptions in the amounts of $26.2 billion,

$79.2 billion, and $16.8 billion, respectively – all decreased amounts compared to 2017.

13

As shown in Table 3, net operating cost includes an adjustment for unmatched transactions and balances, which represent unreconciled differences in

intragovernmental activity and balances between federal entities. These amounts are described in greater detail in the Other Information section of this

Financial Report.

MANAGEMENT’S DISCUSSION AND ANALYSIS

16

o These actuarial estimates and the resulting gains or losses from changes in assumptions can sometimes

cause significant swings in total entity costs from year to year. For example, for fiscal year 2018, changes

in net cost at VA ($132.8 billion decrease), OPM ($66.2 billion decrease), and DOD ($33.0 billion

increase), were impacted by the corresponding changes in gains or losses from assumption changes at these

entities.

• At DOD

, the $33.0 billion net cost

increase includes the net effect of a $39.2

billion decrease in earned revenues across

the department, as well as increases in the

net costs of procurement, military

personnel and research and development

(R&D). These increases were partially

offset by a decrease in losses from

changes in assumptions referenced above

(net cost decrease), and a decrease in costs

of military operations, readiness, and

support;

• $56.4 billion and $39.5 billion net cost

increases at HHS and the

Social Security

Administration (SSA), respectively, were

primarily due to cost increases of the

benefits programs that these entities

administer (HHS – Medicare and

Medicaid programs, SSA – Old-Age,

Survivors, and Disability Insurance

(OASDI) programs);

• A $99.6 billion net cost increase at DOE

largely due to refined environmental

liability estimates, including those for

Waste Treatment and Immobilization

Plant construction, operating costs, tank

farm retrieval, and closure costs at DOE’s

Hanford site;

• A $20.2 billion net cost decrease at the

Pension Benefit Guaranty Corporation

(PBGC) stems mostly from higher interest

rate factors used to measure liabilities for

the single- and multi-employer programs;

and

• A $61.0 billion cost increase in interest on

debt held by the public due largely to an

increase in the debt and average interest rates, as well as inflation adjustments on certain Treasury securities. Interest

costs have increased by 20.6 percent in 2018 from 2017 and

by 37.4 percent over the past five years.

Chart B shows the composition of the government’s net cost. In fiscal year 2018, nearly three fourths of total net

cost came from HHS, SSA, DOD, and VA. Interest on Treasury securities (i.e., debt) held by the public contributed an

additional 8 percent, and the other entities included in the government’s fiscal year 2018 Statement of Net Cost

accounted for a combined 21 percent of the government’s total net cost for fiscal year 2018. Chart C shows the five-year

trend in these costs. These entities have consistently incurred the largest entity shares of the government’s total net cost

in recent years. As indicated above, HHS and SSA net costs for fiscal year 2018 ($1.1 trillion and $1.0 trillion,

respectively) are attributable to major social insurance programs administered by these entities. DOD net costs of $698.4

billion relate primarily to operations, readiness, and support; personnel; research; procurement; and retirement and health

benefits. VA costs of $346.9 billion support health, education and other benefits programs for our nation’s veterans. The

$132.8 billion decrease in VA net cost during fiscal year 2018 is primarily due to the decrease in losses from changes in

actuarial assumptions as referenced earlier. From Chart C, over the past five years, HHS, SSA, and Interest costs have

increased 20.1 percent, 14.6 percent, and 37.4 percent, respectively.

B

17

MANAGEMENT’S DISCUSSION AND ANALYSIS

Tax and Other Revenues

As noted earlier, tax and other revenues from the Statement of Operations and Changes in Net Position are deducted

from total net cost to derive the government’s

“bottom line” net operating cost. Chart D shows

that total tax and other revenue increased slightly

by $9.7 billion or 0.3 percent to $3.4 trillion for

fiscal year 2018. This increase is attributable

mainly to an overall growth in individual income

tax collections, partially offset by reduced estate

and corporate income tax collections and deposit of

earnings from the FR System.

14

Earned revenues

from Table 3 are not considered “taxes and other

revenue” and, thus, are not shown in Chart D.

Individual income tax and tax withholdings and

corporate income taxes accounted for about 82.5

percent and 6.2 percent of total revenue,

respectively in fiscal year 2018; other revenues

from Chart D include Federal Reserve earnings,

excise taxes, unemployment taxes, and customs

duties.

As previously shown in Table 3, the increases in net cost and tax and revenues almost entirely offset each other,

resulting in the government’s bottom line net operating cost remaining largely unchanged at $1.2 trillion for fiscal year 2018.

Tax Expenditures

Tax and other revenues reported reflect the effects of tax expenditures, which are special exclusions, exemptions,

deductions, tax credits, preferential tax rates, and tax deferrals that allow individuals and businesses to reduce taxes they may

otherwise owe. Tax expenditures may be viewed as alternatives to other policy instruments, such as spending or regulatory

programs. For example, the government supports college attendance through both spending programs and tax expenditures.

The government uses Pell Grants to help low- and moderate-income students afford college and allows certain funds used to

meet college expenses to grow tax free in special college savings accounts. Tax expenditures may include deductions and

exclusions which reduce the amount of income subject to tax (e.g., deductions for personal residence mortgage interest). Tax

credits, which reduce tax liability dollar for dollar for the amount of credit (e.g., child tax credit), are also considered tax

expenditures. Tax expenditures may also allow taxpayers to defer tax liability.

Receipts in the calculation of surplus or deficit, and tax revenues in the calculation of net position, reflect the effect of

tax expenditures. As discussed in more detail in the Other Information section of this Financial Report, tax expenditures will

generally lower federal government receipts although tax expenditure estimates do not necessarily equal the increase in

Federal revenues (or the change in the budget balance) that would result from repealing these special provisions.

Tax expenditures are reported annually in the Analytical Perspectives of the Budget. In addition, current and past tax

expenditure estimates and descriptions can be found at the following location from the U.S. Treasury’s Office of Tax Policy:

https://home.treasury.gov/policy-issues/tax-policy/tax-expenditures

.

14

Fiscal year 2018 Department of the Treasury Agency Financial Report, p. 37

MANAGEMENT’S DISCUSSION AND ANALYSIS

18

Assets and Liabilities

The government’s net position at the end of the year is derived by netting the government’s assets against its liabilities,

as presented in the Balance Sheet (summarized in Table 4). The Balance Sheet does not include the financial value of the

government’s sovereign powers to tax, regulate commerce, or set monetary policy or value of nonoperational resources of the

government, such as national and natural resources, for which the government is a steward. In addition, as is the case with the

Statement of Operations and Changes in Net Position, the Balance Sheet includes a separate presentation of the portion of net

position related to funds from dedicated collections. Moreover, the government’s exposures are broader than the liabilities

presented on the Balance Sheet. The government’s future social insurance exposures (e.g., Medicare and Social Security) as

well as other fiscal projections, commitments and contingencies, are reported in separate statements and disclosures. This

information is discussed later in this MD&A section, the financial statements, and RSI sections of this Financial Report.

Assets

As of September 30, 2018, the government’s $3.8 trillion in assets are comprised mostly of net loans receivable ($1.4

trillion) and net property, plant, and equipment (PP&E) ($1.1 trillion).

15

From Financial Statement Note 4, The Department

of Education’s (Education’s) Federal Direct Student Loan Program accounted for $1.1 trillion (78.6 percent) of total net loans

receivable. Education’s direct student loan program receivables balances have grown by more than 190 percent since fiscal

year 2011 largely due to increased direct loan disbursements, attributable to the continued effect of 2010 legislation requiring

a transition for new loans from guaranteed student loans to full direct lending by Education.

16

15

For financial reporting purposes, other than multi-use heritage assets, stewardship assets of the government are not recorded as part of Property, Plant, and

Equipment. Stewardship assets are comprised of stewardship land and heritage assets. Stewardship land consists of public domain land (e.g., national parks,

wildlife refuges). Heritage assets include national monuments and historical sites that among other characteristics are of historical, natural, cultural,

educational, or artistic significance. See Note 24 – Stewardship Land and Heritage Assets.

16

With the enactment of the SAFRA Act, which was included as part of the Health Care and Education Reconciliation Act of 2010 (HCERA) (P. L. 111-

152), no new loans were originated under the Federal Family Education Loan (FFEL) Program (guaranteed loan program) since July 1, 2010. See

Department of Education fiscal year 2018 Agency Financial Report

p. 50.

19

MANAGEMENT’S DISCUSSION AND ANALYSIS

Liabilities

As indicated in Table 4 and Chart E, of the

government’s $25.4 trillion in total liabilities, the

largest liability is federal debt securities held by the

public and accrued interest, the balance of which

increased by $1.1 trillion (7.4 percent) to $15.8

trillion as of September 30, 2018.

The other major component of the

government’s liabilities is federal employee and

veteran benefits payable (i.e., the government’s

pension and other benefit plans for its military and

civilian employees), which increased $282.2 billion

(3.7 percent) during fiscal year 2018, to about $8.0

trillion. This total amount is comprised of $2.5

trillion in benefits payable for the current and

retired civilian workforce, and $5.4 trillion for the

military and veterans. OPM administers the largest

civilian pension plan, covering nearly 2.7 million

current employees and 2.6 million annuitants and

survivors. The military pension plan covers about

2.1 million current military personnel (including active service, reserve, and National Guard) and approximately 2.3 million

retirees and survivors.

Federal Debt

The budget surplus or deficit is the difference between total federal spending and receipts (e.g., taxes) in a given year.

The government borrows from the public (increases federal debt levels) to finance deficits. During a budget surplus (i.e.,

when receipts exceed spending), the government typically uses those excess funds to reduce the debt held by the public. The

Statement of Changes in Cash Balance from Budget and Other Activities reports how the annual budget surplus or deficit

relates to the federal government’s borrowing and changes in cash and other monetary assets. It also explains how a budget

surplus or deficit normally affects changes in debt balances.

The government’s publicly-held debt, or federal debt held by the public, and accrued interest (Balance Sheet liability)

totaled $15.8 trillion as of September 30, 2018. It is comprised of Treasury securities, such as bills, notes, and bonds, net of

unamortized discounts and premiums; and accrued interest payable. The “public” consists of individuals, corporations, state

and local governments, Federal Reserve Banks (FRBs), foreign governments, and other entities outside the federal

government. As indicated above, budget surpluses have typically resulted in borrowing reductions, and budget deficits have

conversely yielded borrowing increases. However, the government’s debt operations are generally much more complex. Each

year, trillions of dollars of debt mature and new debt is issued to take its place. In fiscal year 2018, new borrowings were

$10.1 trillion, and repayments of maturing debt held by the public were $9.0 trillion, both increases from fiscal year 2017.

MANAGEMENT’S DISCUSSION AND ANALYSIS

20

Prior to 1917, Congress approved each debt

issuance. In 1917, to facilitate planning in World

War I, Congress and the President established a

dollar ceiling for federal borrowing. With the

Public Debt Act of 1941 (Public Law [P.L.] 77-7),

Congress and the President set an overall limit of

$65 billion on Treasury debt obligations that

could be outstanding at any one time. Since then,

Congress and the

President have enacted a

number of measures affecting the debt limit,

including several in recent years. Congress and

the President most recently suspended the debt

limit from February 9, 2018 through March 1,

2019. It is important to note that increasing or

suspending the debt limit does not increase

spending or authorize new spending; rather, it

permits the United States to continue to honor

pre-

existing commitments to its citizens,

businesses, and investors domestically and around

the world.

In addition to debt held by the public, the government has

about $5.8 trillion in intragovernmental debt outstanding, which

arises when one part of the government borrows from another. It

represents debt issued by the Treasury and held by government

accounts, including the Social Security ($2.9 trillion) and

Medicare ($301.0 billion) trust funds. Intragovernmental debt is

primarily held in government trust funds in the form of special

nonmarketable securities by various parts of the government.

Laws establishing government trust funds generally require

excess trust fund receipts (including interest earnings) over

disbursements to be invested in these special securities. Because

these amounts are both liabilities of the Treasury and assets of

the government trust funds, they are eliminated as part of the

consolidation process for the governmentwide financial

statements (see Note 11). When those securities are redeemed,

e.g., to pay Social Security benefits, the government will need

to obtain the resources necessary to reimburse the trust funds.

The sum of debt held by the public and intragovernmental debt

equals gross federal debt, which (with some adjustments), is

subject to a statutory ceiling (i.e., the debt limit). At the end of

fiscal year 2018, debt subject to the statutory limit (DSL) was

$21.5 trillion

17

(see sidebar).

The federal debt held by the public measured as a percent of GDP (debt-to-GDP ratio) (Chart F) compares the country’s

debt to the size of its economy, making this

measure sensitive to changes in both. Over time,

the debt-to-GDP ratio has varied widely:

• For most of the nation’s history,

through the first half of the 20

th

century,

the debt-to-GDP ratio has tended to

increase during wartime and decline

during peacetime.

• Chart F shows that wartime spending

and borrowing pushed the debt-to-GDP

ratio to an all-time high of 106 percent

in 1946, soon after the end of World

War II, but it decreased rapidly in the

post-war years,

• The ratio grew rapidly from the mid-

1970s until the early 1990s. Strong

economic growth and fundamental

fiscal decisions, including measures to

reduce the federal deficit and

implementation of binding "Pay As You

Go" (PAYGO) rules (which require that

new tax or spending laws not add to the deficit), generated a significant decline in the debt-to-GDP ratio, from a

peak of 48 percent in 1993-1995, to 31 percent in 2001.

• During the first decade of the 21

st

century, PAYGO rules were allowed to lapse, significant tax cuts were

implemented, entitlements were expanded, and spending related to defense and homeland security increased. By

September 2008, the debt-to-GDP ratio was 39 percent of GDP.

• PAYGO rules were reinstated in 2010, but the extraordinary demands of the last economic and fiscal crisis and the

consequent actions taken by the federal government, combined with slower economic growth in the wake of the

crisis, pushed the debt-to-GDP ratio up to 74 percent by the end of fiscal year 2014.

• The debt was 78.0 percent of GDP at the end of fiscal year 2018 (compared to 76 percent at the end of fiscal year

2017).

18